| Global Leader in Small Satellites |

| Eric Leeds Head of Investor Relations Welcome |

| Chris Hollod Co-CEO & Director, Tailwind Two |

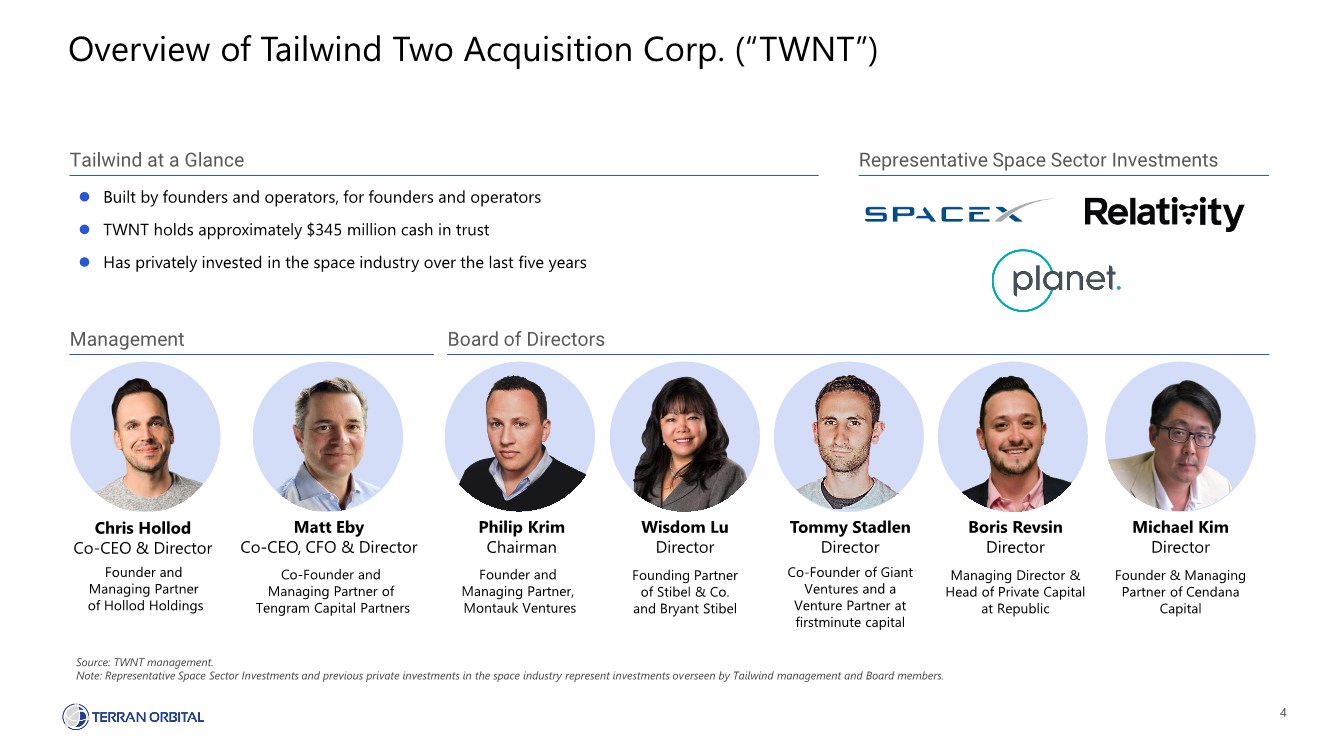

| 4 Overview of Tailwind Two Acquisition Corp. (“TWNT”) Founder and Managing Partner of Hollod Holdings Chris Hollod Co-CEO & Director Co-Founder and Managing Partner of Tengram Capital Partners Matt Eby Co-CEO, CFO & Director Founder and Managing Partner, Montauk Ventures Philip Krim Chairman Founding Partner of Stibel & Co. and Bryant Stibel Wisdom Lu Director Co-Founder of Giant Ventures and a Venture Partner at firstminute capital Tommy Stadlen Director Managing Director & Head of Private Capital at Republic Boris Revsin Director Founder & Managing Partner of Cendana Capital Michael Kim Director ⚫ Built by founders and operators, for founders and operators ⚫ TWNT holds approximately $345 million cash in trust ⚫ Has privately invested in the space industry over the last five years Tailwind at a Glance Management Board of Directors Representative Space Sector Investments Source: TWNT management. Note: Representative Space Sector Investments and previous private investments in the space industry represent investments overseen by Tailwind management and Board members. |

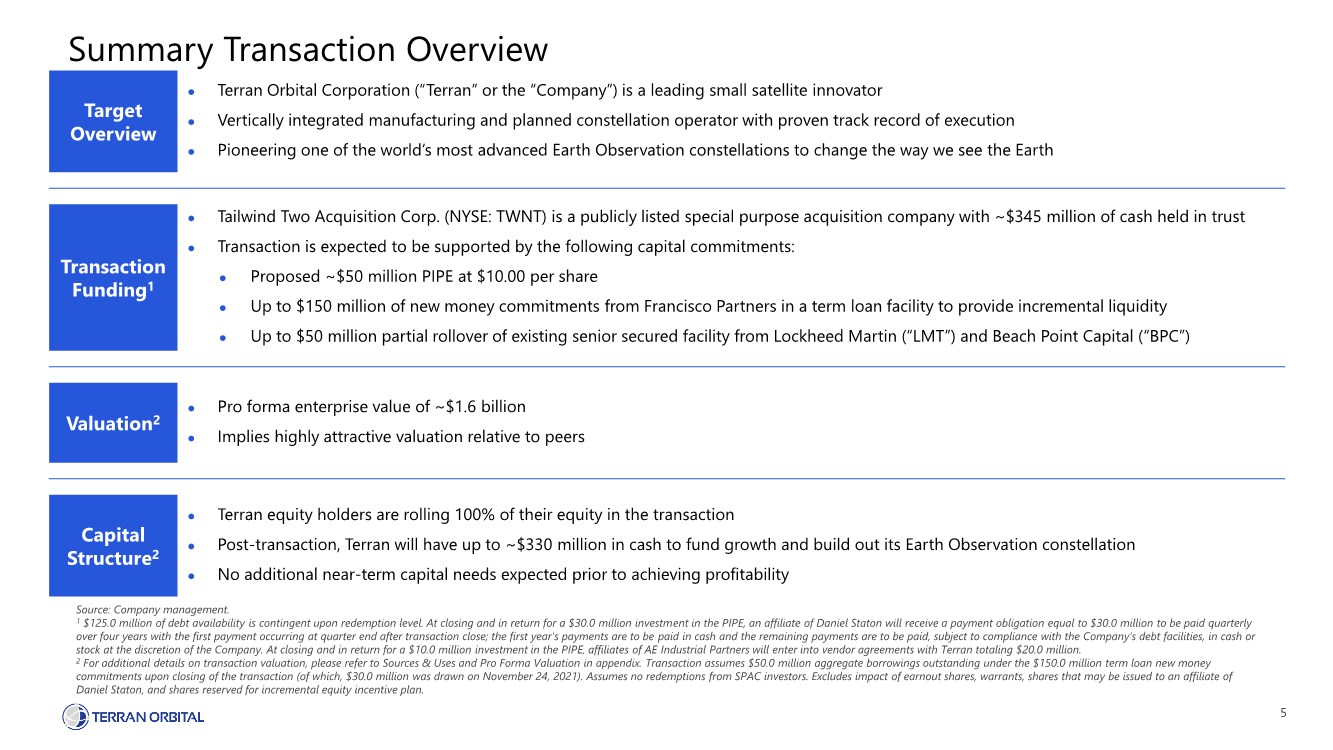

| 5 Summary Transaction Overview Source: Company management. 1 $125.0 million of debt availability is contingent upon redemption level. At closing and in return for a $30.0 million investment in the PIPE, an affiliate of Daniel Staton will receive a payment obligation equal to $30.0 million to be paid quarterly over four years with the first payment occurring at quarter end after transaction close; the first year's payments are to be paid in cash and the remaining payments are to be paid, subject to compliance with the Company’s debt facilities, in cash or stock at the discretion of the Company. At closing and in return for a $10.0 million investment in the PIPE, affiliates of AE Industrial Partners will enter into vendor agreements with Terran totaling $20.0 million. 2 For additional details on transaction valuation, please refer to Sources & Uses and Pro Forma Valuation in appendix. Transaction assumes $50.0 million aggregate borrowings outstanding under the $150.0 million term loan new money commitments upon closing of the transaction (of which, $30.0 million was drawn on November 24, 2021). Assumes no redemptions from SPAC investors. Excludes impact of earnout shares, warrants, shares that may be issued to an affiliate of Daniel Staton, and shares reserved for incremental equity incentive plan. Target Overview ⚫ Terran Orbital Corporation (“Terran” or the “Company”) is a leading small satellite innovator ⚫ Vertically integrated manufacturing and planned constellation operator with proven track record of execution ⚫ Pioneering one of the world’s most advanced Earth Observation constellations to change the way we see the Earth Transaction Funding1 ⚫ Tailwind Two Acquisition Corp. (NYSE: TWNT) is a publicly listed special purpose acquisition company with ~$345 million of cash held in trust ⚫ Transaction is expected to be supported by the following capital commitments: ⚫ Proposed ~$50 million PIPE at $10.00 per share ⚫ Up to $150 million of new money commitments from Francisco Partners in a term loan facility to provide incremental liquidity ⚫ Up to $50 million partial rollover of existing senior secured facility from Lockheed Martin (“LMT”) and Beach Point Capital (“BPC”) Valuation2 ⚫ Pro forma enterprise value of ~$1.6 billion ⚫ Implies highly attractive valuation relative to peers Capital Structure2 ⚫ Terran equity holders are rolling 100% of their equity in the transaction ⚫ Post-transaction, Terran will have up to ~$330 million in cash to fund growth and build out its Earth Observation constellation ⚫ No additional near-term capital needs expected prior to achieving profitability |

| Marc Bell Co-Founder, Chairman & Chief Executive Officer |

| 7 7 Explorer 1 (1958): First NASA Satellite Source: NASA. 7 |

| 8 8 USA 213 Launched 2010 3,600 pounds Satellites Became Larger & More Expensive USA 213 – 3,600 Pounds (Launched 2010). Source: NASA, USAF. Vanguard 1 – 3 Pounds (Launched 1958). 8 |

| 9 9 9 Source: Various. Satellite Applications Enable Many Modern Conveniences |

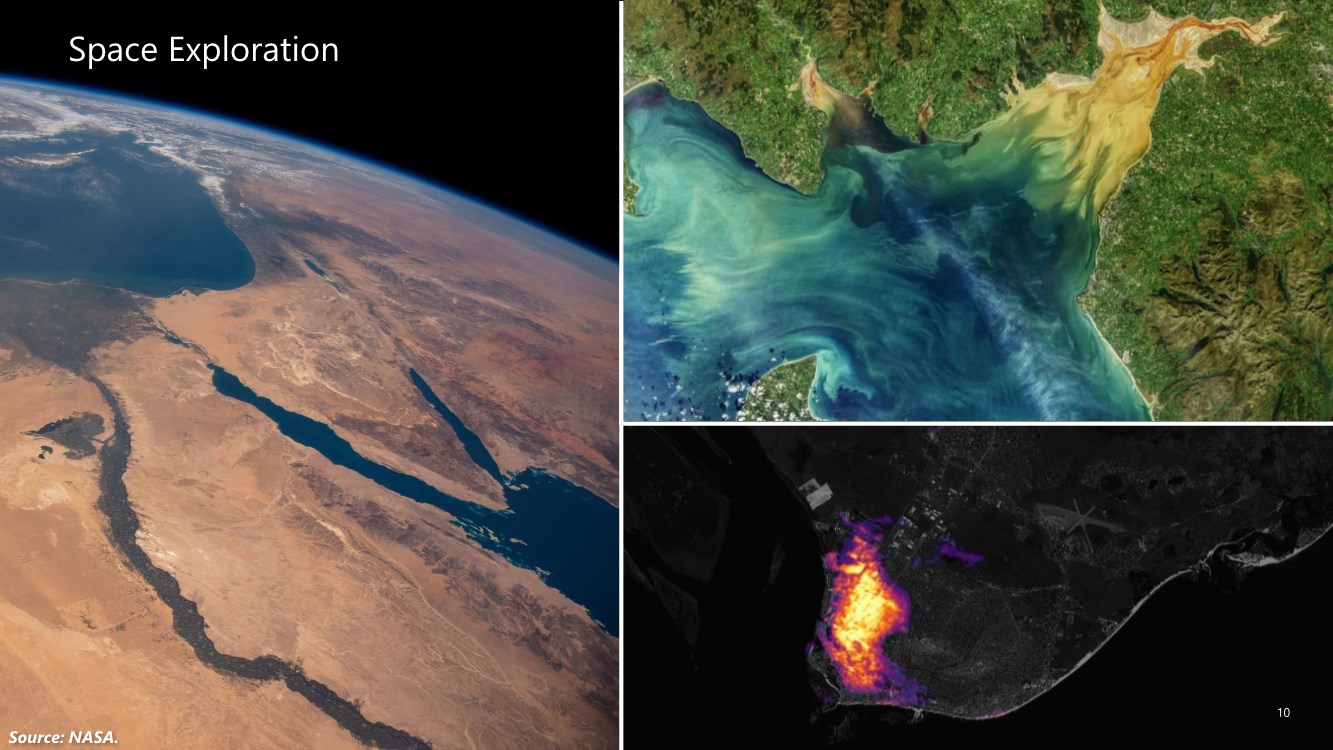

| 1010 Source: NASA. Space Exploration 10 |

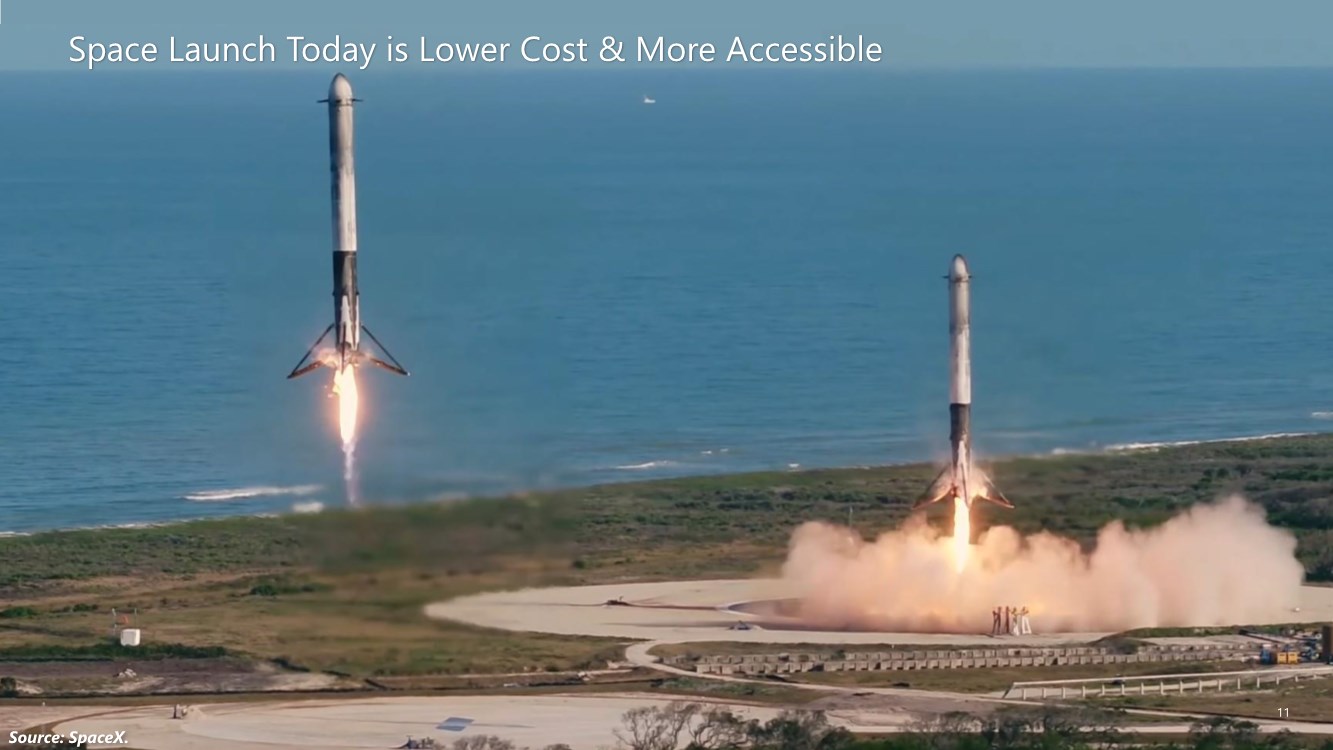

| 1111 Source: SpaceX. Space Launch Today is Lower Cost & More Accessible 11 |

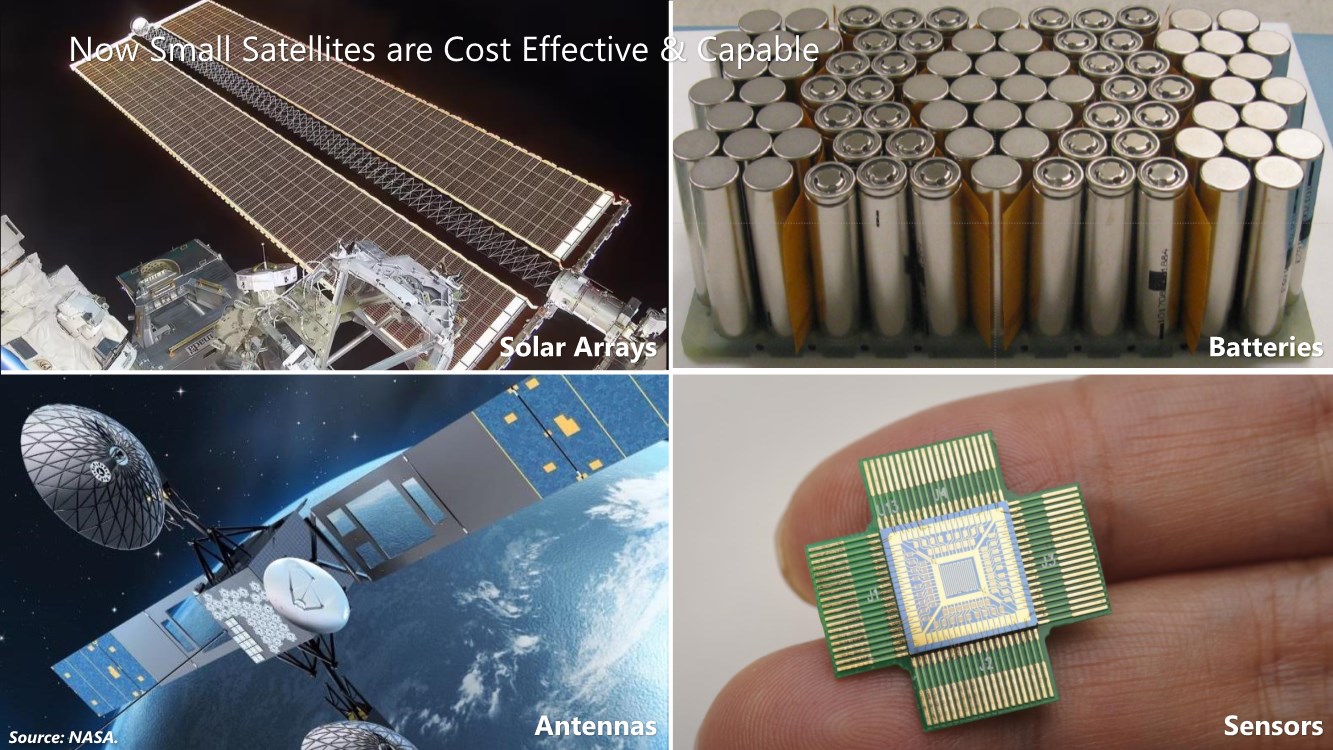

| 12 Now Small Satellites are Cost Effective & Capable Source: NASA. Sensors Batteries Antennas Solar Arrays |

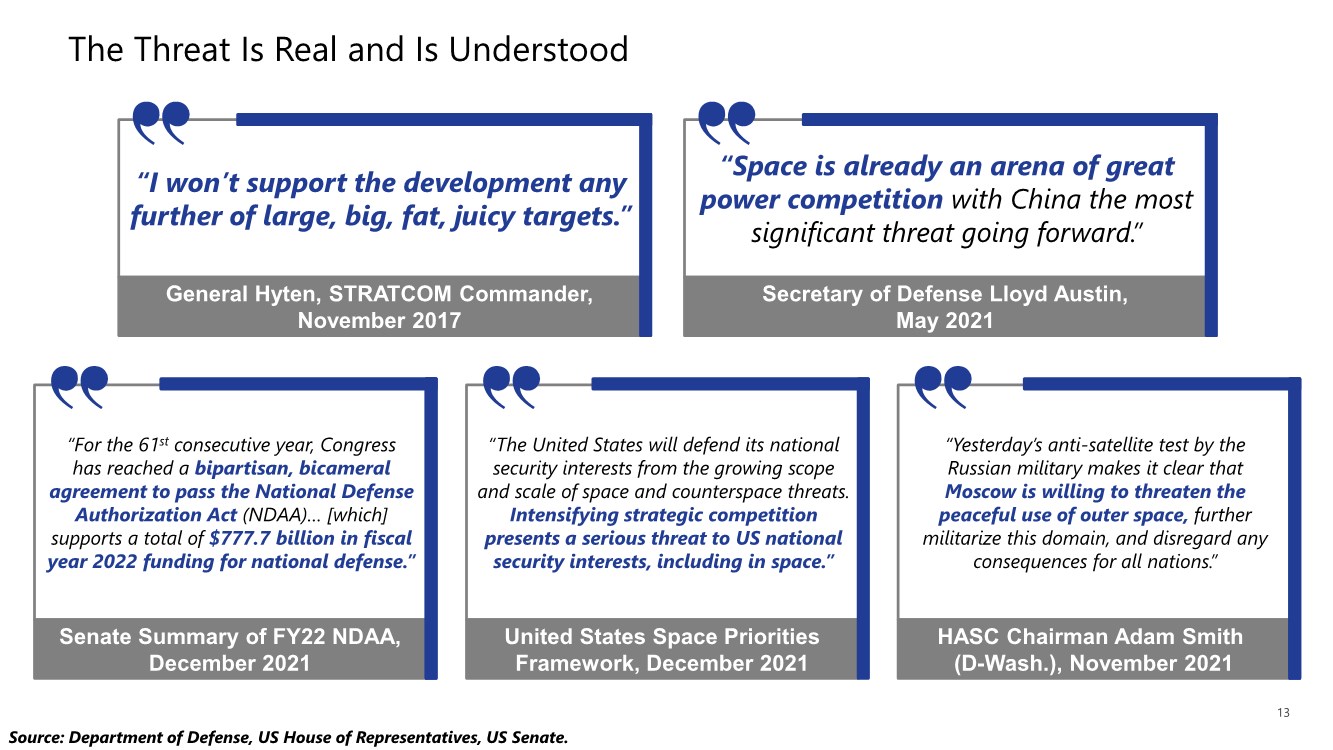

| 13 The Threat Is Real and Is Understood Source: Department of Defense, US House of Representatives, US Senate. “The United States will defend its national security interests from the growing scope and scale of space and counterspace threats. Intensifying strategic competition presents a serious threat to US national security interests, including in space.” United States Space Priorities Framework, December 2021 “Yesterday’s anti-satellite test by the Russian military makes it clear that Moscow is willing to threaten the peaceful use of outer space, further militarize this domain, and disregard any consequences for all nations.” HASC Chairman Adam Smith (D-Wash.), November 2021 “For the 61st consecutive year, Congress has reached a bipartisan, bicameral agreement to pass the National Defense Authorization Act (NDAA)… [which] supports a total of $777.7 billion in fiscal year 2022 funding for national defense.” Senate Summary of FY22 NDAA, December 2021 “I won’t support the development any further of large, big, fat, juicy targets.” General Hyten, STRATCOM Commander, November 2017 “Space is already an arena of great power competition with China the most significant threat going forward.” Secretary of Defense Lloyd Austin, May 2021 |

| 14 Source: Space Development Agency. 14 Space Development Agency Established to Acquire Small Satellite Constellations |

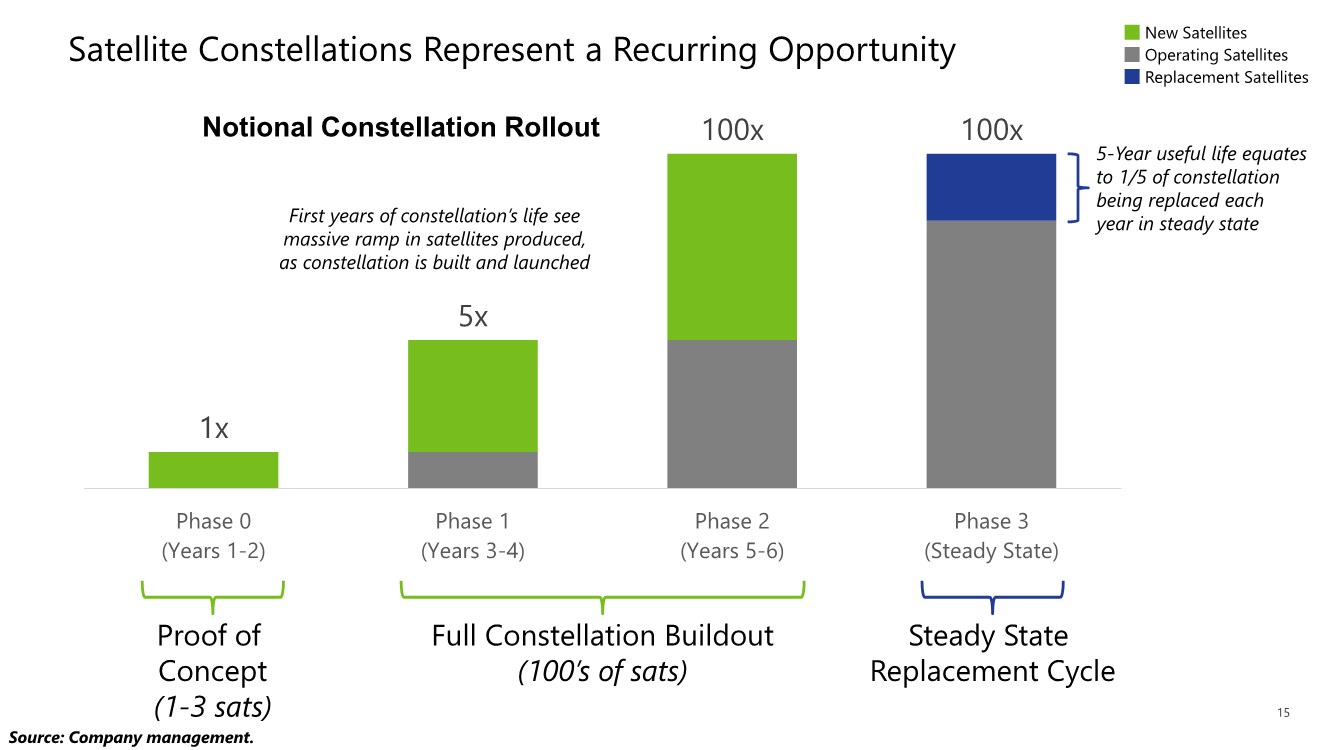

| 15 Satellite Constellations Represent a Recurring Opportunity 15 1x 5x 100x 100x Phase 0 (Years 1-2) Phase 1 (Years 3-4) Phase 2 (Years 5-6) Phase 3 (Steady State) Operating Satellites New Satellites Replacement Satellites Proof of Concept (1-3 sats) Source: Company management. 5-Year useful life equates to 1/5 of constellation being replaced each year in steady state First years of constellation’s life see massive ramp in satellites produced, as constellation is built and launched Full Constellation Buildout (100’s of sats) Steady State Replacement Cycle Notional Constellation Rollout |

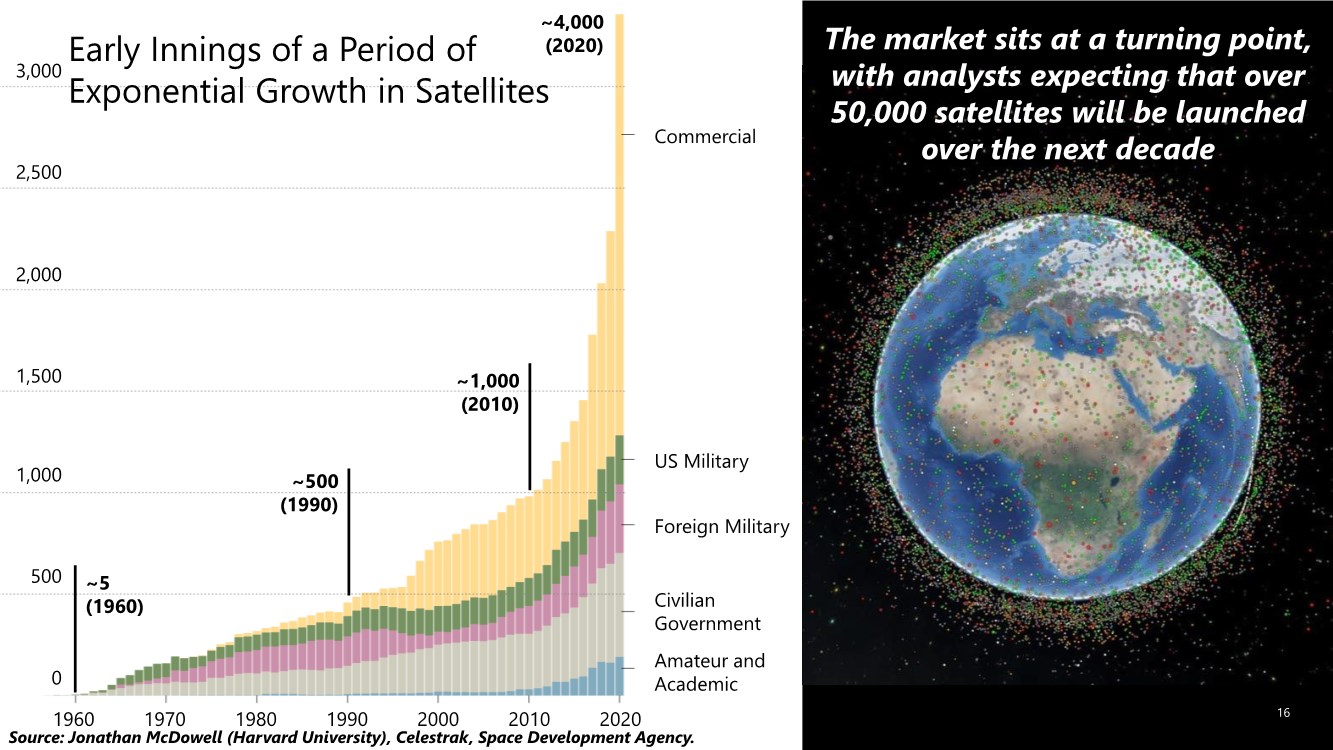

| 16 3,000 2,500 2,000 1,500 1,000 500 0 Commercial US Military Foreign Military Civilian Government Amateur and Academic Early Innings of a Period of Exponential Growth in Satellites Source: Jonathan McDowell (Harvard University), Celestrak, Space Development Agency. 1960 1970 1980 1990 2000 2010 2020 The market sits at a turning point, with analysts expecting that over 50,000 satellites will be launched over the next decade 16 ~5 (1960) ~500 (1990) ~1,000 (2010) ~4,000 (2020) |

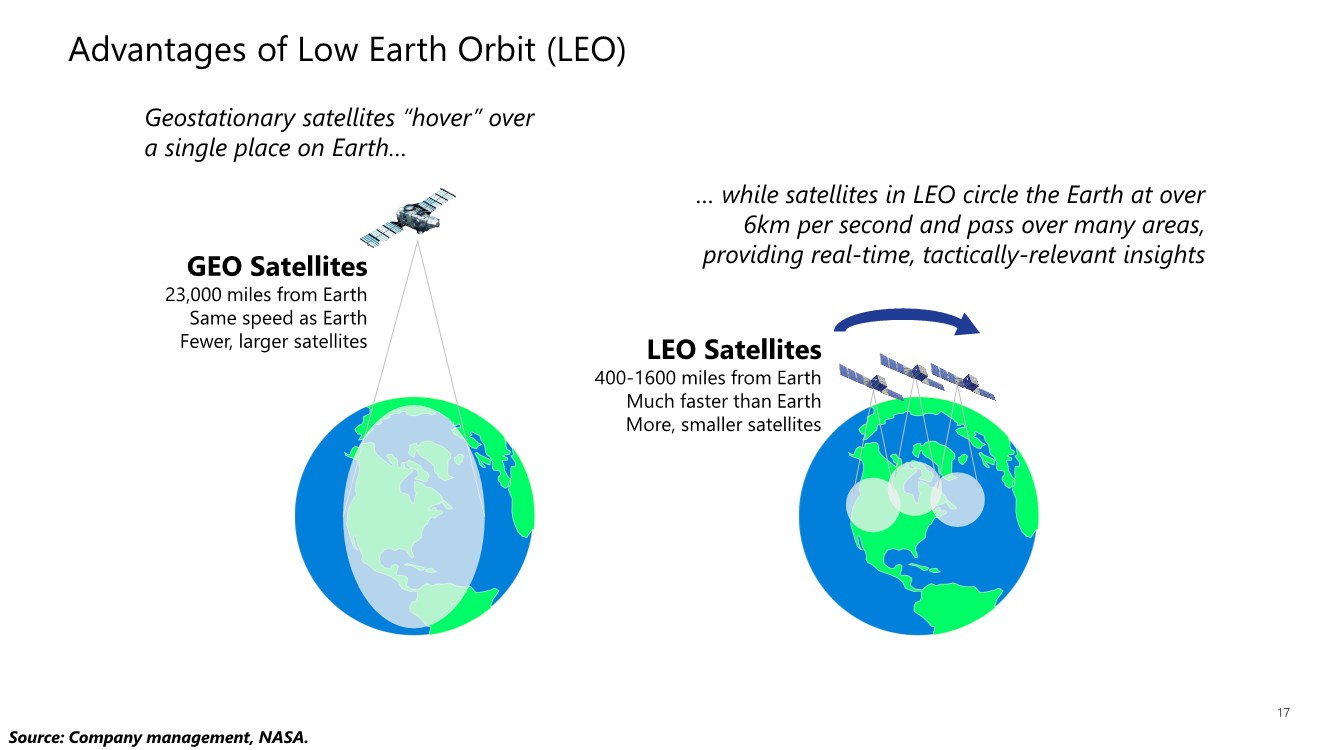

| 17 Advantages of Low Earth Orbit (LEO) 17 GEO Satellites 23,000 miles from Earth Same speed as Earth Fewer, larger satellites LEO Satellites 400-1600 miles from Earth Much faster than Earth More, smaller satellites Source: Company management, NASA. Geostationary satellites “hover” over a single place on Earth… … while satellites in LEO circle the Earth at over 6km per second and pass over many areas, providing real-time, tactically-relevant insights |

| 18 Source: California Polytechnic State University, NASA. We Invented CubeSats 18 |

| 19 Rendering of Proposed Terran Facility in Florida. Source: Company management. 19 Terran Orbital Plans to Industrialize Small Satellite Manufacturing |

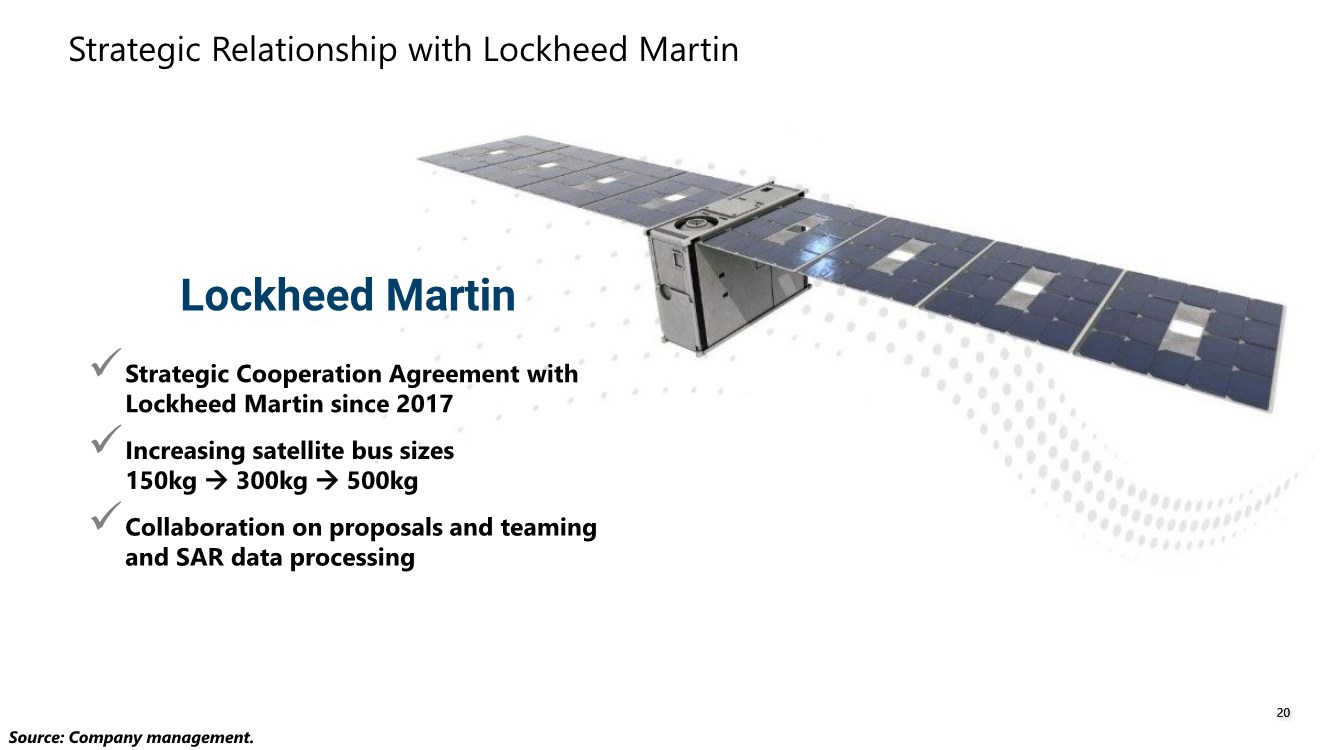

| 20 Strategic Relationship with Lockheed Martin Source: Company management. 20 ✓Strategic Cooperation Agreement with Lockheed Martin since 2017 ✓Increasing satellite bus sizes 150kg → 300kg → 500kg ✓Collaboration on proposals and teaming and SAR data processing Lockheed Martin |

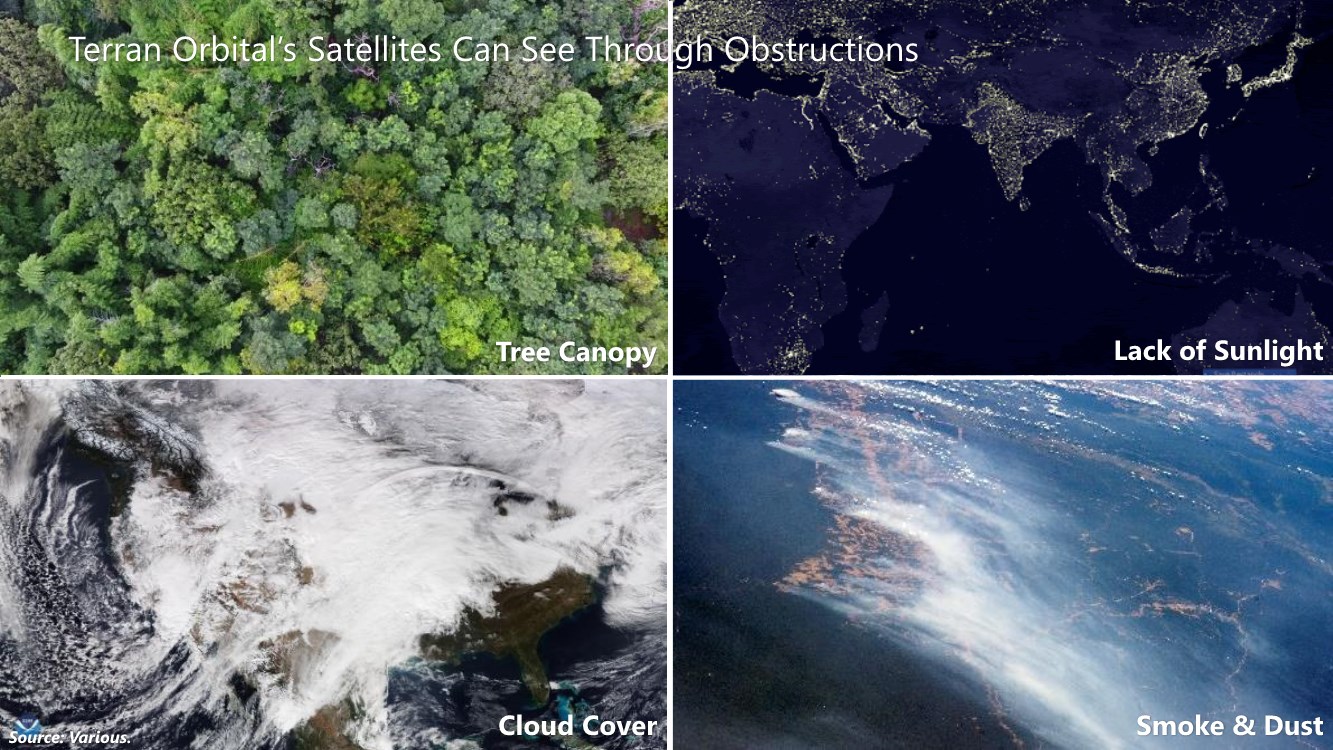

| 21 Smoke & Dust Lack of Sunlight Tree Canopy Cloud Cover Terran Orbital’s Satellites Can See Through Obstructions Source: Various. |

| 2222 Source: NASA. Satellite Earth Observation Use Cases |

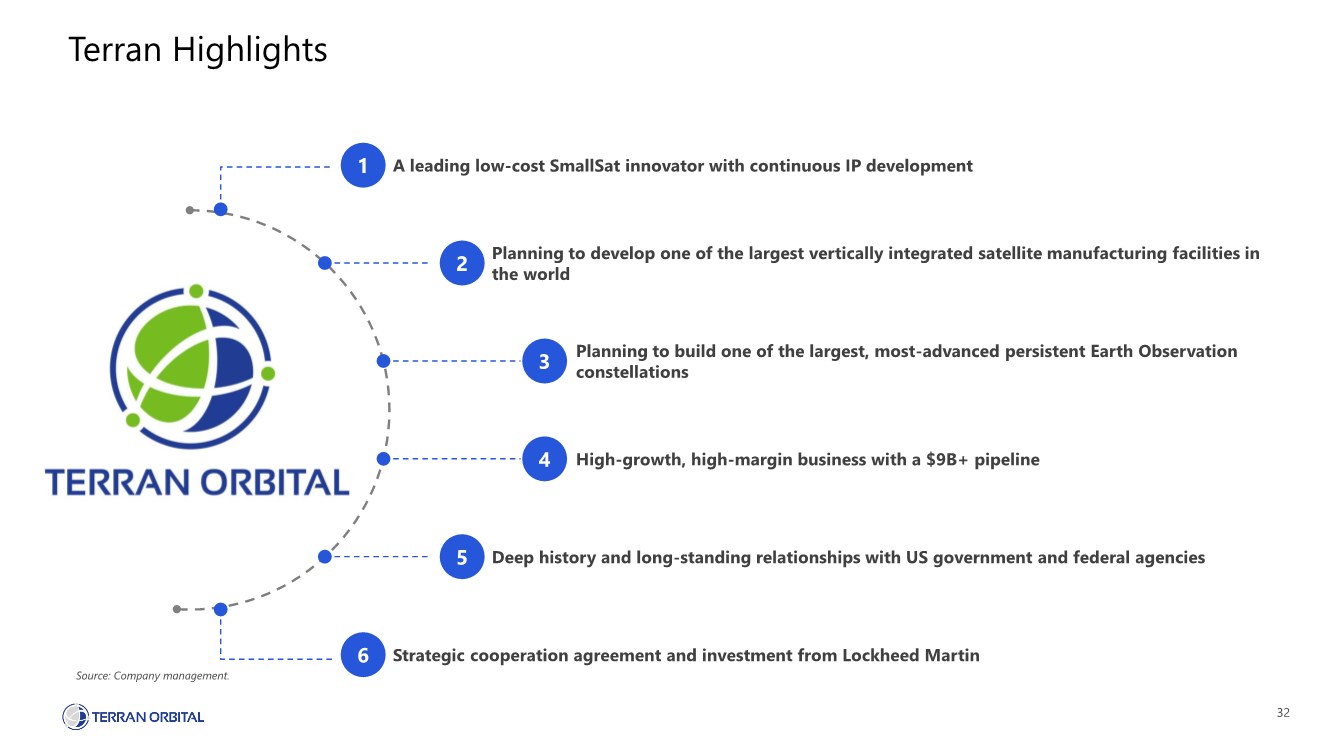

| 23 Terran Orbital Highlights 1. A leading low-cost SmallSat innovator with continuous IP development 2. Planning to develop one of the largest vertically integrated satellite manufacturing facilities in the world 3. Planning to build one of the largest, most-advanced persistent Earth Observation constellations 4. High-growth, high-margin business with a $9B+ pipeline 5. Deep history and long-standing relationships with US government and federal agencies 6. Strategic cooperation agreement and investment from Lockheed Martin Source: Company management. 23 |

| 24 Recent Award and Business Momentum Source: Company management. Terran Orbital’s Global Headcount Increased from 200+ to Nearly 300 Since October 2021 Terran Orbital Announces a Record $170+ Million in New Contracts and Awards Since September 30, 2021 Terran Orbital to Significantly Expand Manufacturing Capability in Irvine, CA ✓ ✓ ✓ |

| 25 Proven Track-Record of Designing, Executing and Operating in Space World Class Management Team Source: Company management. Note: Please refer to the Appendix for full management biographies. Marc Bell Co-Founder, Chairman & Chief Executive Officer Tony Previte Co-Founder & Chief Strategy Officer Marco Villa Executive Vice President & Chief Revenue Officer Gary Hobart Chief Financial Officer Maj Gen Roger Teague, USAF (Ret.) President, Defense and Intelligence Systems RADM Christian “Boris” Becker, USN (Ret.) President, Satellite Solutions LTG Dave Mann, USA (Ret.) Vice President, Strategy, Army Systems & Defense Programs Eric Truitt Chief Solutions Officer Hilary Hageman General Counsel Eric Leeds Head of Investor Relations |

| Marco Villa Executive Vice President & Chief Revenue Officer |

| 27 Building One of the Most Advanced Earth Observation Constellations Source: Company management. A Global Leader in Small Satellites |

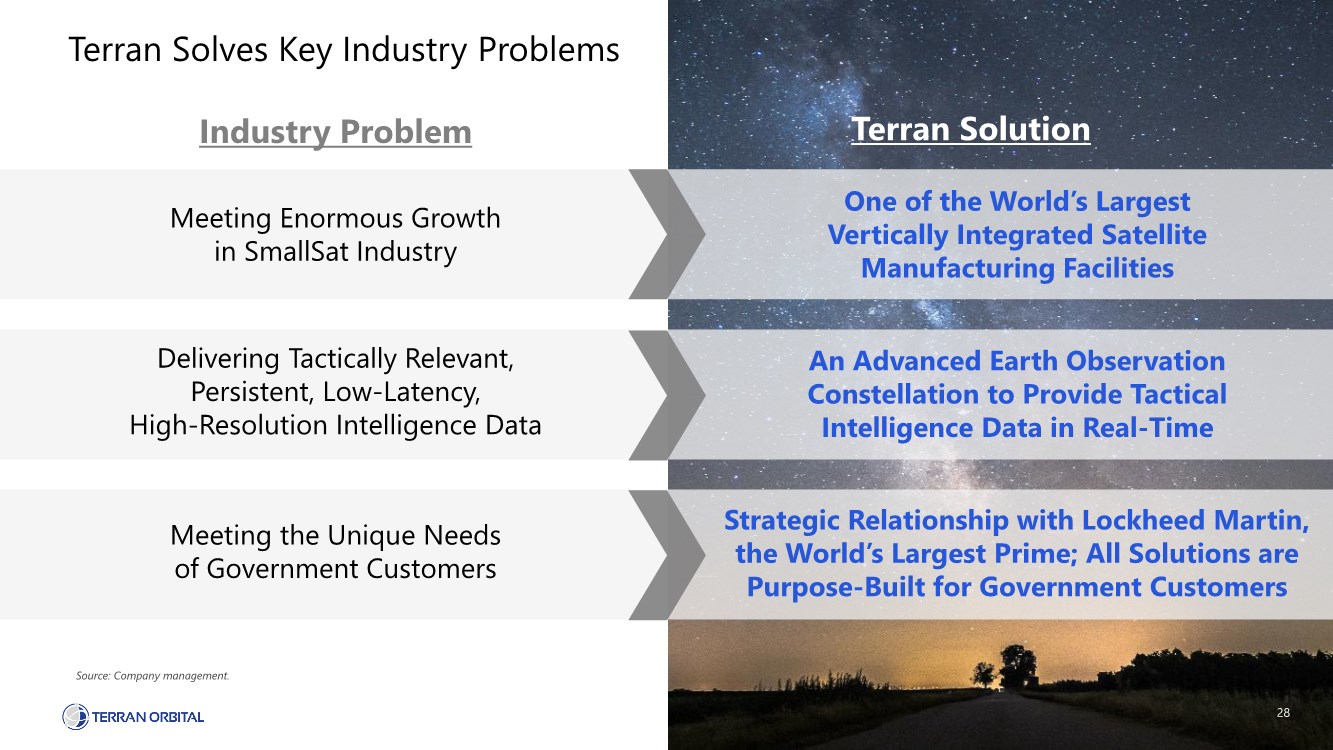

| 28 28 Terran Solves Key Industry Problems Meeting Enormous Growth in SmallSat Industry Industry Problem Terran Solution One of the World’s Largest Vertically Integrated Satellite Manufacturing Facilities Meeting the Unique Needs of Government Customers Strategic Relationship with Lockheed Martin, the World’s Largest Prime; All Solutions are Purpose-Built for Government Customers Delivering Tactically Relevant, Persistent, Low-Latency, High-Resolution Intelligence Data An Advanced Earth Observation Constellation to Provide Tactical Intelligence Data in Real-Time Source: Company management. |

| 29 Proposed State-of-the-Art Manufacturing Facility Expansions in California and Florida Terran expects to take advantage of economies of scale with its proposed Florida facility, reducing the cost and time to manufacture its state-of-the-art satellites Rendering of Proposed Terran Facility in Florida. Source: Company management. ~660,000 sq. ft. proposed facility on the Space Coast of Florida 10 satellite manufacturing lines >1,000 estimated annual SmallSat throughput ~60,000 sq. ft. facility expansion in California 2x represents more than 2x in near term capacity expansion ~53,000 sq. ft. current manufacturing capacity globally 29 |

| 30 TAM >$340B Over Next 5 Years Source: Company management; Frost & Sullivan "Global Satellite Manufacturing Growth Opportunities;" Euroconsult “The Space Economy Report, 2019;” and Euroconsult “Earth Observation Data & Services Market, 13th Edition.” Note: Total addressable market consists of satellite design & production (representing satellite manufacturing), mission operations (representing satellite operations), and Earth Observation (representing commercial Earth Observation market). 1 TAM statistics are implied based on current market size and ’21 –’26 CAGR, assuming identical annual growth for each year. Terran Segment Market Design & Production Mission Operations Earth Observation TAM1 $190B+ ’21 -’26 $115B+ ’21 -’26 $35B+ ’21 -’26 Vertically Integrated Provider of Satellite Solutions One of the World’s Most Advanced Earth Observation Satellite Constellations Microsats Nanosats Manufacturing Mission Operations Launch Services Per Image Data-as-a-Service Subscription Raw Data Big Data Persistent Global Coverage |

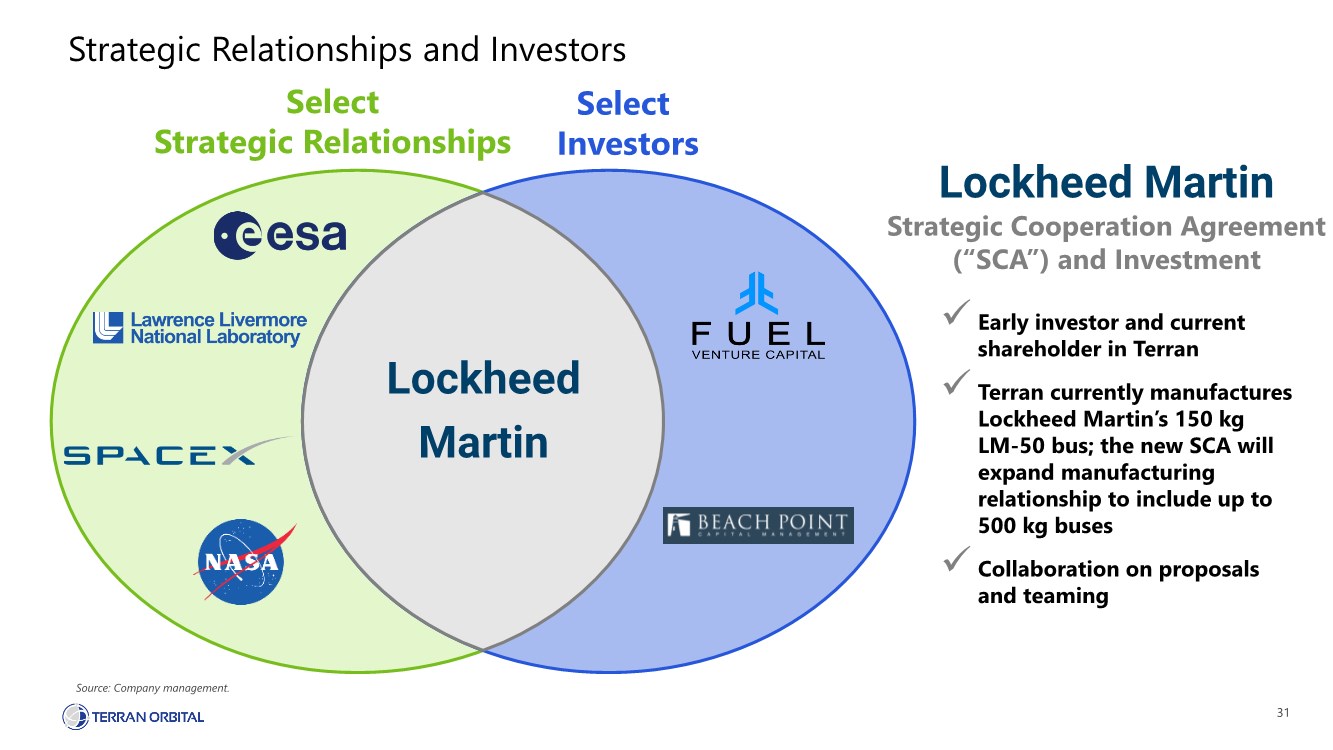

| 31 Strategic Relationships and Investors Select Strategic Relationships Select Investors Strategic Cooperation Agreement (“SCA”) and Investment ✓ Early investor and current shareholder in Terran ✓ Terran currently manufactures Lockheed Martin’s 150 kg LM-50 bus; the new SCA will expand manufacturing relationship to include up to 500 kg buses ✓ Collaboration on proposals and teaming Source: Company management. Lockheed Martin Lockheed Martin |

| 32 Terran Highlights A leading low-cost SmallSat innovator with continuous IP development Planning to develop one of the largest vertically integrated satellite manufacturing facilities in the world Planning to build one of the largest, most-advanced persistent Earth Observation constellations High-growth, high-margin business with a $9B+ pipeline Deep history and long-standing relationships with US government and federal agencies Strategic cooperation agreement and investment from Lockheed Martin 1 2 3 4 5 6 Source: Company management. |

| Vertically Integrated Provider of Satellite Solutions RADM Christian “Boris” Becker, USN (Ret.) President, Satellite Solutions |

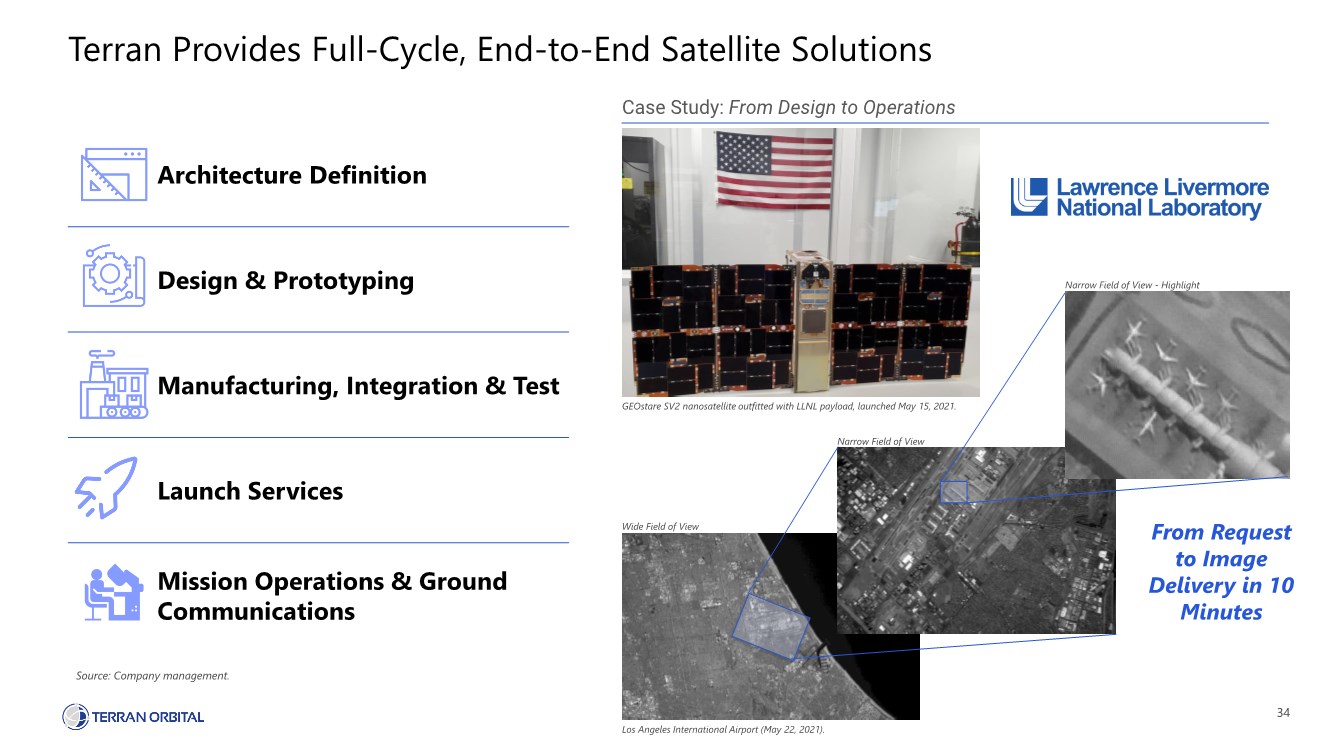

| 34 Architecture Definition Design & Prototyping Manufacturing, Integration & Test Launch Services Mission Operations & Ground Communications Terran Provides Full-Cycle, End-to-End Satellite Solutions Source: Company management. GEOstare SV2 nanosatellite outfitted with LLNL payload, launched May 15, 2021. Case Study: From Design to Operations Wide Field of View Narrow Field of View Narrow Field of View - Highlight From Request to Image Delivery in 10 Minutes Los Angeles International Airport (May 22, 2021). |

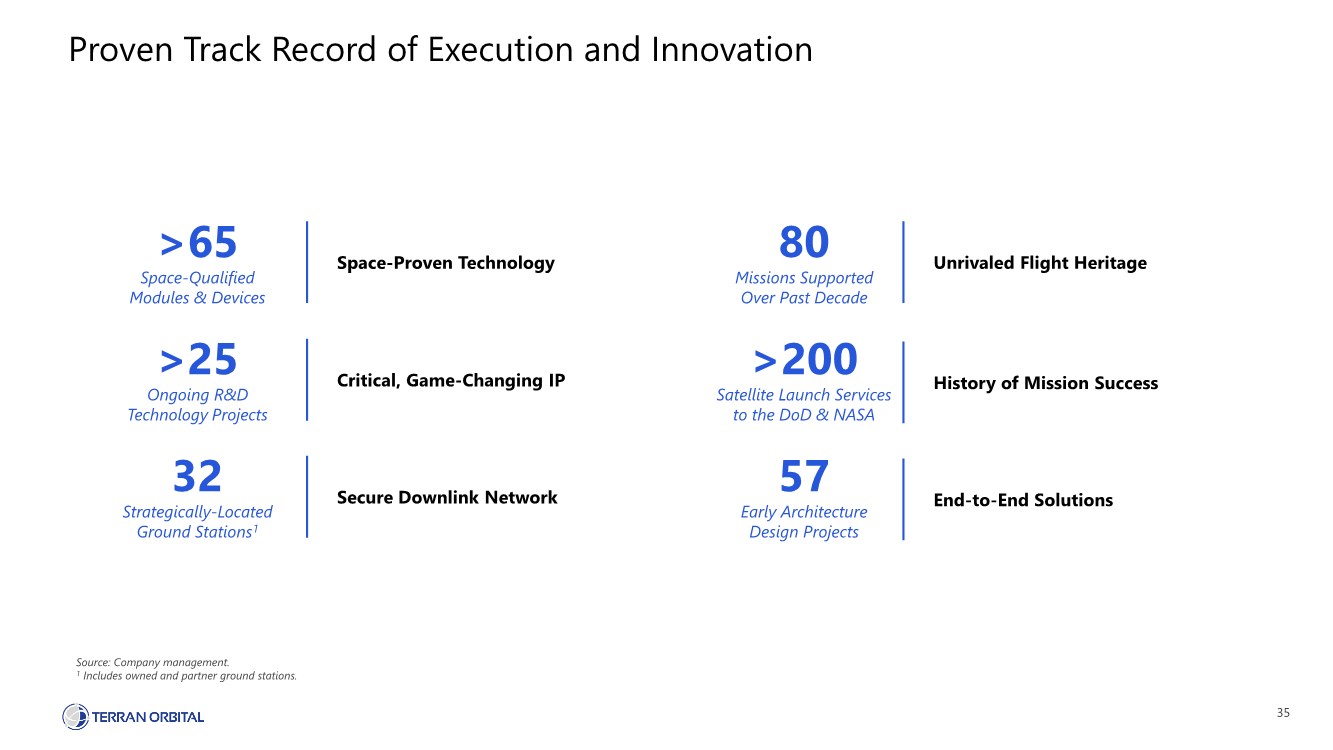

| 35 Proven Track Record of Execution and Innovation Source: Company management. 1 Includes owned and partner ground stations. Unrivaled Flight Heritage 80 Missions Supported Over Past Decade End-to-End Solutions 57 Early Architecture Design Projects Space-Proven Technology >65 Space-Qualified Modules & Devices Critical, Game-Changing IP >25 Ongoing R&D Technology Projects Secure Downlink Network 32 Strategically-Located Ground Stations1 History of Mission Success >200 Satellite Launch Services to the DoD & NASA |

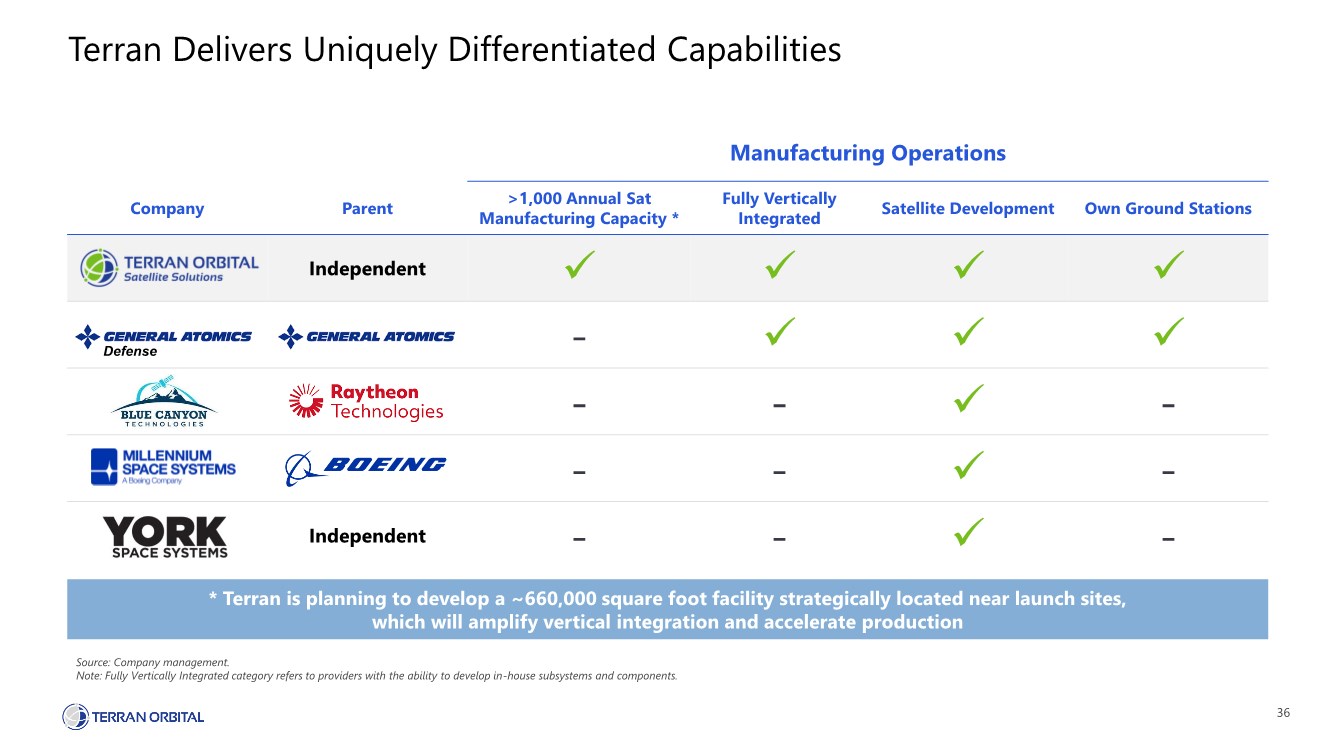

| 36 Source: Company management. Note: Fully Vertically Integrated category refers to providers with the ability to develop in-house subsystems and components. Terran Delivers Uniquely Differentiated Capabilities * Terran is planning to develop a ~660,000 square foot facility strategically located near launch sites, which will amplify vertical integration and accelerate production Manufacturing Operations Company Parent >1,000 Annual Sat Manufacturing Capacity * Fully Vertically Integrated Satellite Development Own Ground Stations Independent ✓ ✓ ✓ ✓ - ✓ ✓ ✓ -- ✓ - -- ✓ - Independent -- ✓ - Defense |

| 37 Capability Layers The US Space Development Agency Plans to Acquire Many Satellites 37 Space Development Agency ⚫ Founded in 2019, the Space Development Agency will partner with commercial providers to procure and proliferate new space solutions quickly and efficiently ⚫ The SDA has announced plans to launch “layers“ of small satellites, with hundreds of small satellites per layer Source: Space Development Agency. Transport Battle Management Tracking Custody Emerging Capabilities Navigation Support The Space Development Agency’s Notional Architecture |

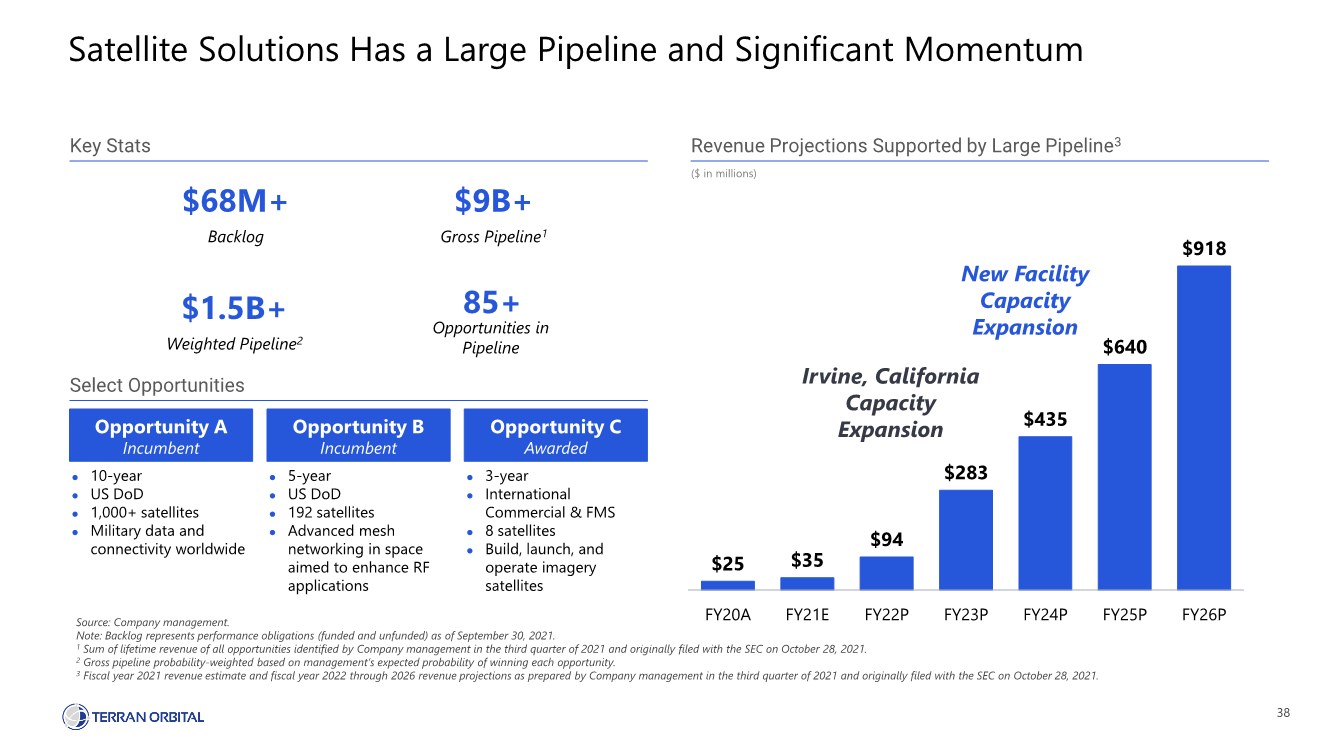

| 38 Satellite Solutions Has a Large Pipeline and Significant Momentum Key Stats Select Opportunities Opportunity A Incumbent ⚫ 10-year ⚫ US DoD ⚫ 1,000+ satellites ⚫ Military data and connectivity worldwide Opportunity B Incumbent ⚫ 5-year ⚫ US DoD ⚫ 192 satellites ⚫ Advanced mesh networking in space aimed to enhance RF applications Opportunity C Awarded ⚫ 3-year ⚫ International Commercial & FMS ⚫ 8 satellites ⚫ Build, launch, and operate imagery satellites $25 $35 $94 $283 $435 $640 $918 FY20A FY21E FY22P FY23P FY24P FY25P FY26P Backlog $68M+ Gross Pipeline1 $9B+ Weighted Pipeline2 $1.5B+ 85+ Opportunities in Pipeline Irvine, California Capacity Expansion New Facility Capacity Expansion Source: Company management. Note: Backlog represents performance obligations (funded and unfunded) as of September 30, 2021. 1 Sum of lifetime revenue of all opportunities identified by Company management in the third quarter of 2021 and originally filed with the SEC on October 28, 2021. 2 Gross pipeline probability-weighted based on management’s expected probability of winning each opportunity. 3 Fiscal year 2021 revenue estimate and fiscal year 2022 through 2026 revenue projections as prepared by Company management in the third quarter of 2021 and originally filed with the SEC on October 28, 2021. Revenue Projections Supported by Large Pipeline3 ($ in millions) |

| Industry-Leading Earth Observation Satellite Constellation Maj Gen Roger Teague, USAF (Ret.) President, Defense and Intelligence Systems LTG Dave Mann, USA (Ret.) Vice President, Strategy, Army Systems & Defense Programs Eric Truitt Chief Solutions Officer |

| 40 Video: Terran Orbital’s Earth Observation Solutions Business Source: Company management. |

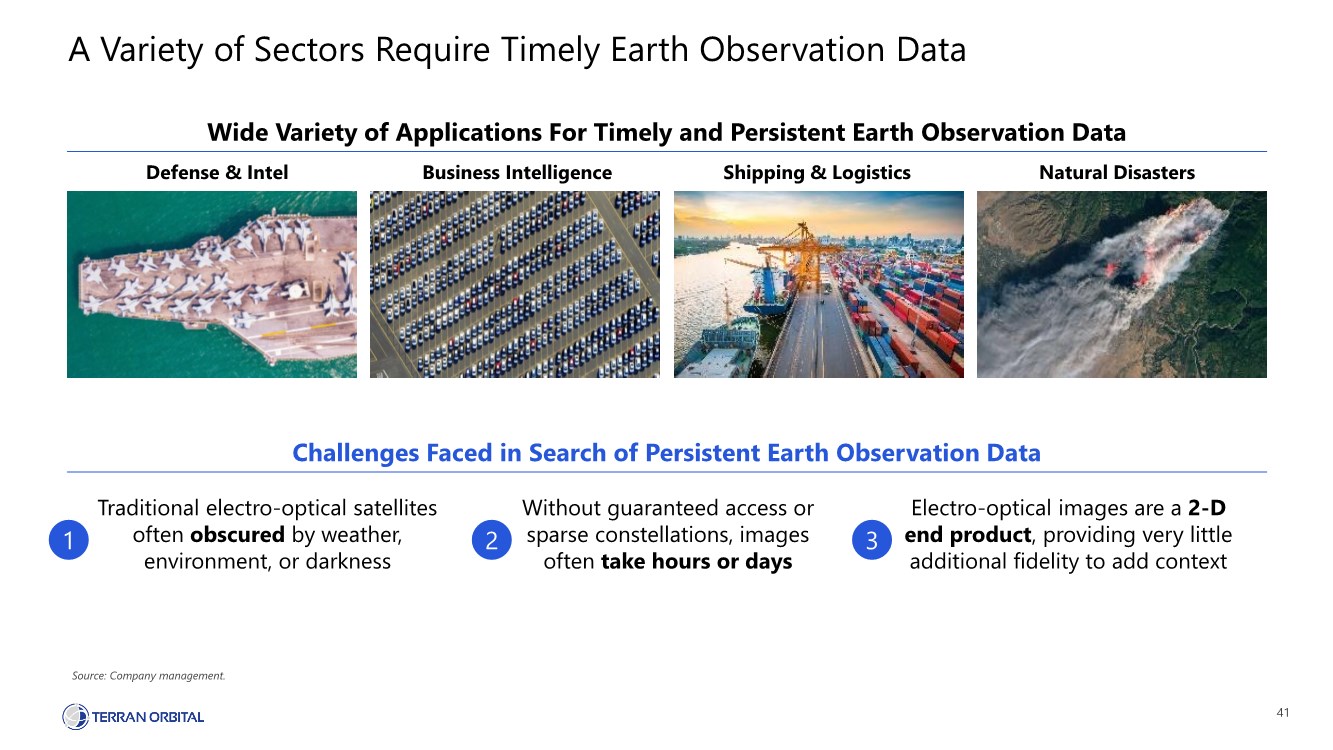

| 41 A Variety of Sectors Require Timely Earth Observation Data Source: Company management. Wide Variety of Applications For Timely and Persistent Earth Observation Data Challenges Faced in Search of Persistent Earth Observation Data Traditional electro-optical satellites often obscured by weather, environment, or darkness Without guaranteed access or sparse constellations, images often take hours or days Electro-optical images are a 2-D end product, providing very little additional fidelity to add context Defense & Intel Business Intelligence Shipping & Logistics Natural Disasters 1 2 3 |

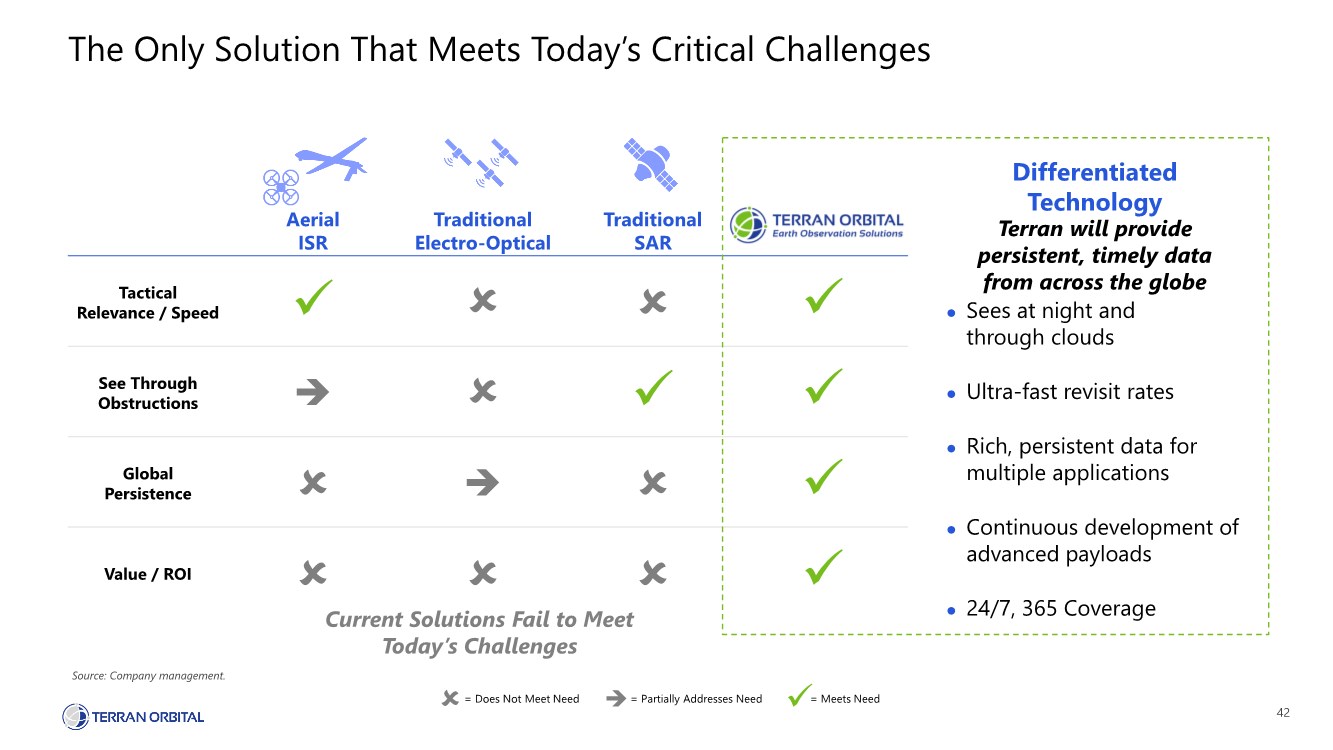

| 42 The Only Solution That Meets Today’s Critical Challenges Source: Company management. Aerial ISR Traditional Electro-Optical Traditional SAR Tactical Relevance / Speed ✓ ✓ See Through Obstructions ➔ ✓ ✓ Global Persistence ➔ ✓ Value / ROI ✓ ⚫ Sees at night and through clouds ⚫ Ultra-fast revisit rates ⚫ Rich, persistent data for multiple applications ⚫ Continuous development of advanced payloads ⚫ 24/7, 365 Coverage Differentiated Technology Terran will provide persistent, timely data from across the globe Current Solutions Fail to Meet Today’s Challenges = Meets Need ✓ = Does Not Meet Need = Partially Addresses Need ➔ |

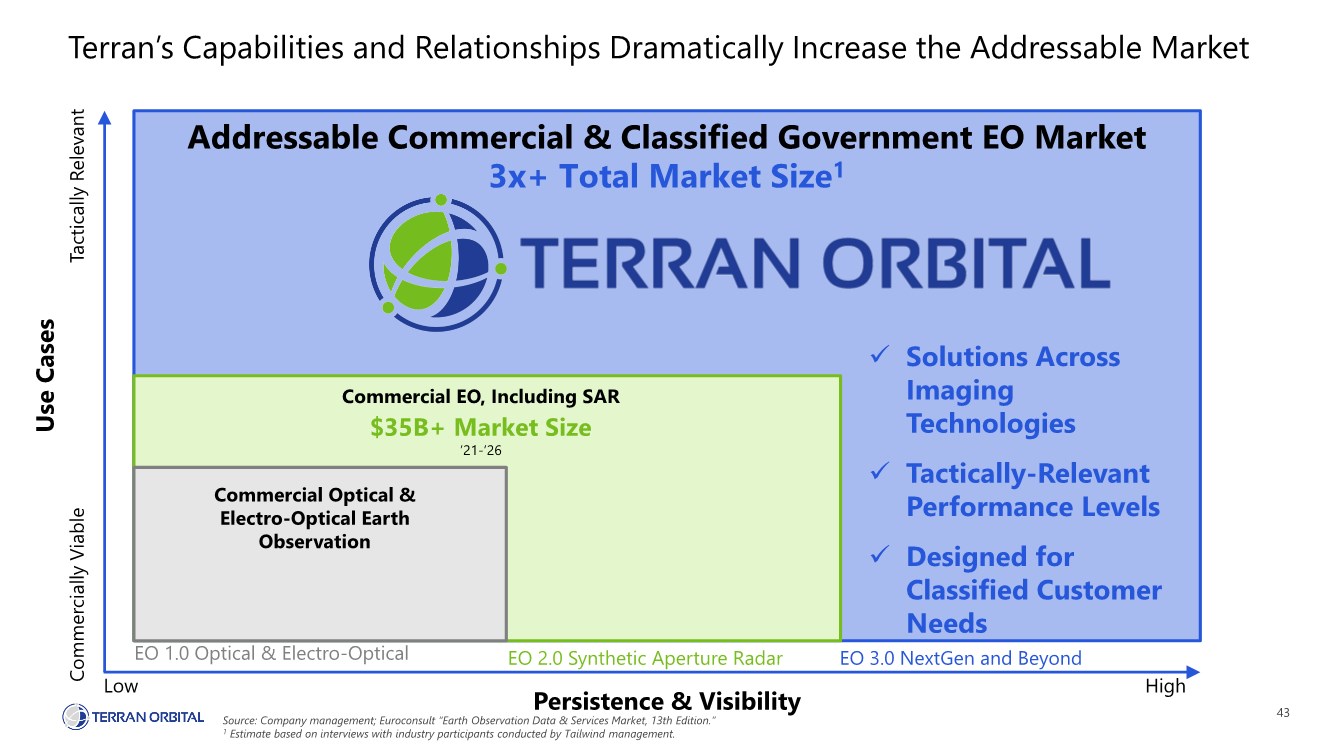

| 43 Terran’s Capabilities and Relationships Dramatically Increase the Addressable Market Addressable Commercial & Classified Government EO Market Commercial EO, Including SAR Commercial Optical & Electro-Optical Earth Observation $35B+ Market Size ’21-’26 ✓ Solutions Across Imaging Technologies ✓ Tactically-Relevant Performance Levels ✓ Designed for Classified Customer Needs 3x+ Total Market Size1 Use Cases Persistence & Visibility Commercially Viable EO 3.0 NextGen and Beyond EO 2.0 Synthetic Aperture Radar EO 1.0 Optical & Electro-Optical High Low Tactically Relevant Source: Company management; Euroconsult “Earth Observation Data & Services Market, 13th Edition.” 1 Estimate based on interviews with industry participants conducted by Tailwind management. |

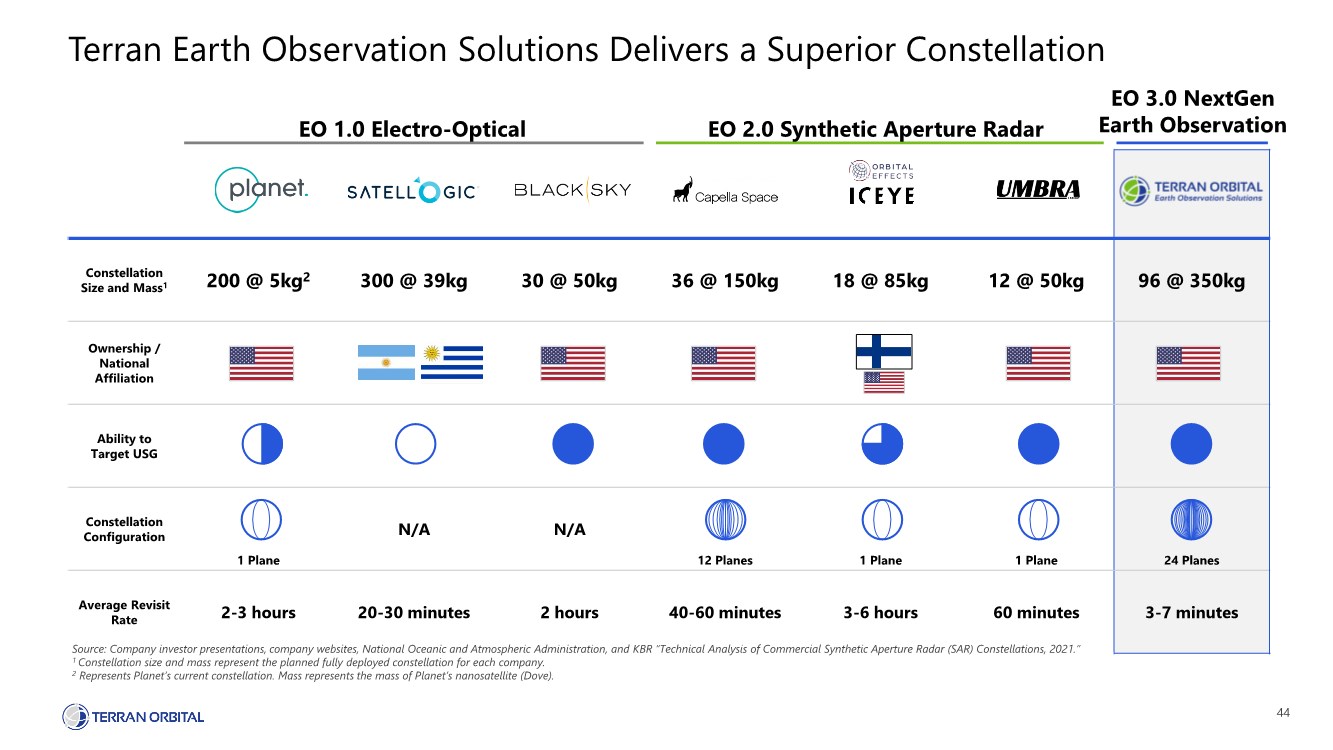

| 44 Constellation Size and Mass1 200 @ 5kg2 300 @ 39kg 30 @ 50kg 36 @ 150kg 18 @ 85kg 12 @ 50kg 96 @ 350kg Ownership / National Affiliation Ability to Target USG Constellation Configuration 1 Plane N/A N/A 12 Planes 1 Plane 1 Plane 24 Planes Average Revisit Rate 2-3 hours 20-30 minutes 2 hours 40-60 minutes 3-6 hours 60 minutes 3-7 minutes Terran Earth Observation Solutions Delivers a Superior Constellation Source: Company investor presentations, company websites, National Oceanic and Atmospheric Administration, and KBR “Technical Analysis of Commercial Synthetic Aperture Radar (SAR) Constellations, 2021.” 1 Constellation size and mass represent the planned fully deployed constellation for each company. 2 Represents Planet’s current constellation. Mass represents the mass of Planet’s nanosatellite (Dove). EO 2.0 Synthetic Aperture Radar EO 1.0 Electro-Optical EO 3.0 NextGen Earth Observation |

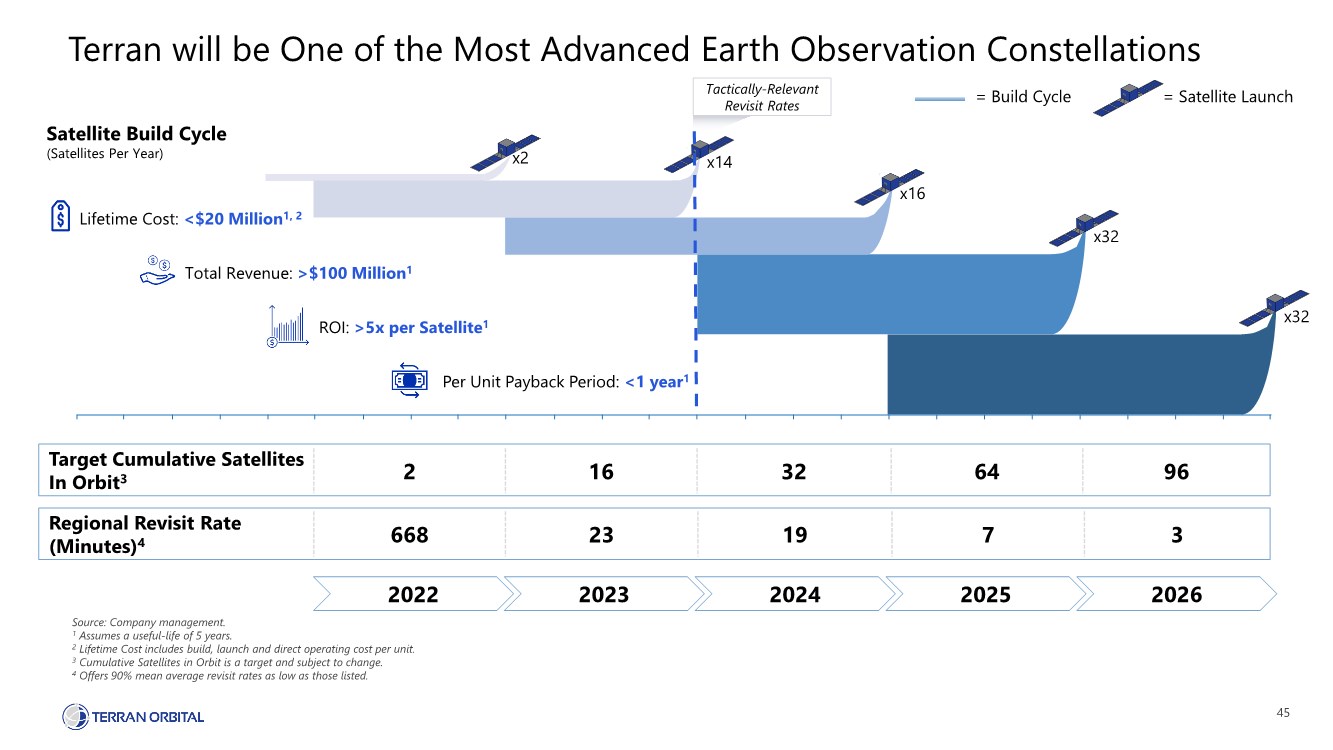

| 45 Satellite Build Cycle (Satellites Per Year) x32 x2 x14 x16 x32 Terran will be One of the Most Advanced Earth Observation Constellations Source: Company management. 1 Assumes a useful-life of 5 years. 2 Lifetime Cost includes build, launch and direct operating cost per unit. 3 Cumulative Satellites in Orbit is a target and subject to change. 4 Offers 90% mean average revisit rates as low as those listed. Regional Revisit Rate (Minutes)4 Target Cumulative Satellites In Orbit3 2 16 32 64 96 2024 2025 2022 2023 668 23 19 7 3 2026 = Satellite Launch = Build Cycle Tactically-Relevant Revisit Rates Per Unit Payback Period: <1 year1 ROI: >5x per Satellite1 Lifetime Cost: <$20 Million1, 2 Total Revenue: >$100 Million1 |

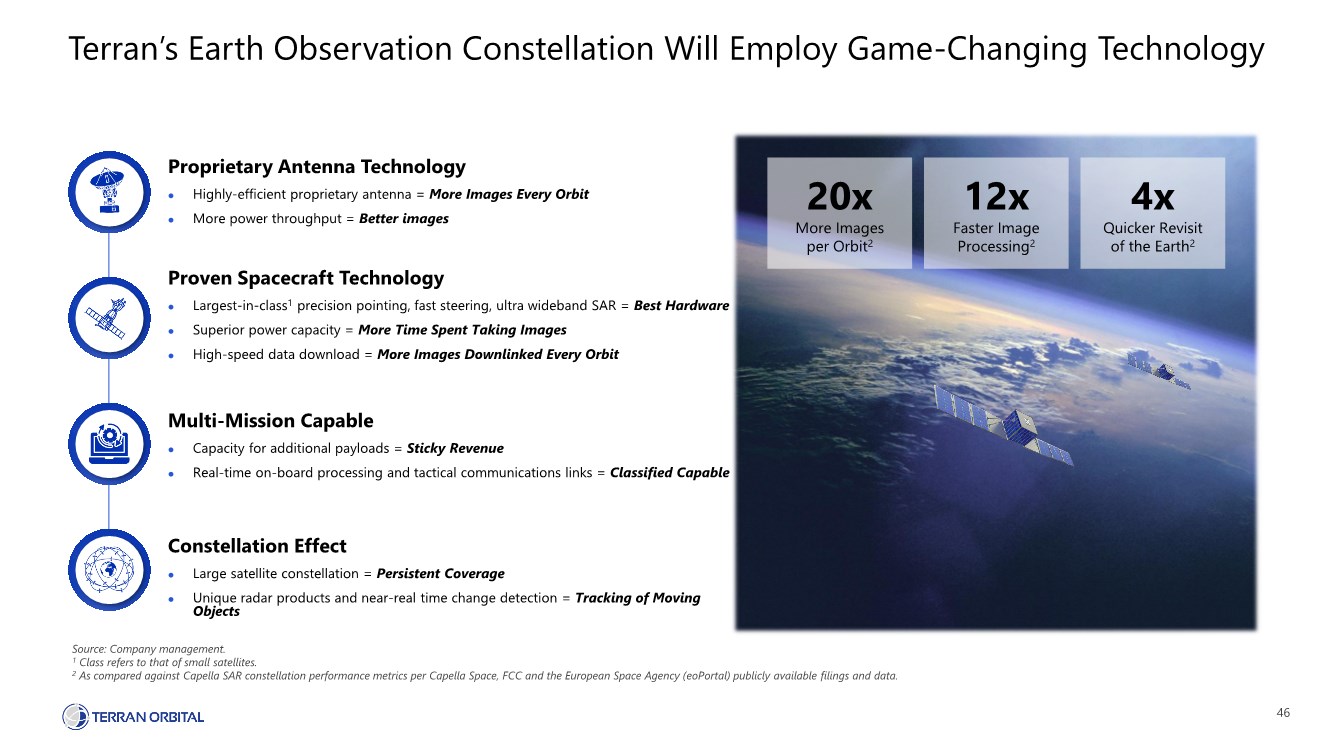

| 46 Terran’s Earth Observation Constellation Will Employ Game-Changing Technology Source: Company management. 1 Class refers to that of small satellites. 2 As compared against Capella SAR constellation performance metrics per Capella Space, FCC and the European Space Agency (eoPortal) publicly available filings and data. Proprietary Antenna Technology ⚫ Highly-efficient proprietary antenna = More Images Every Orbit ⚫ More power throughput = Better images Proven Spacecraft Technology ⚫ Largest-in-class1 precision pointing, fast steering, ultra wideband SAR = Best Hardware ⚫ Superior power capacity = More Time Spent Taking Images ⚫ High-speed data download = More Images Downlinked Every Orbit Multi-Mission Capable ⚫ Capacity for additional payloads = Sticky Revenue ⚫ Real-time on-board processing and tactical communications links = Classified Capable Constellation Effect ⚫ Large satellite constellation = Persistent Coverage ⚫ Unique radar products and near-real time change detection = Tracking of Moving Objects 4x Quicker Revisit of the Earth2 12x Faster Image Processing2 20x More Images per Orbit2 |

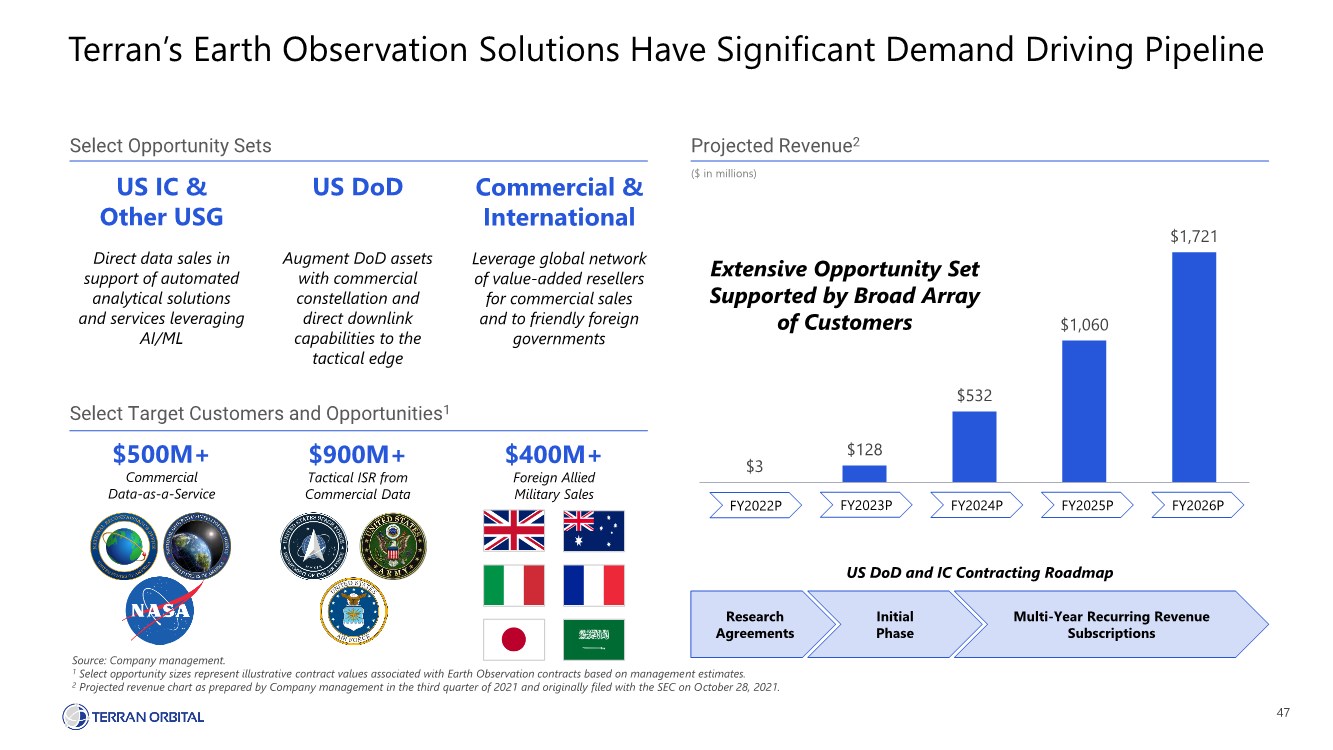

| 47 $3 $128 $532 $1,060 $1,721 Terran’s Earth Observation Solutions Have Significant Demand Driving Pipeline Source: Company management. 1 Select opportunity sizes represent illustrative contract values associated with Earth Observation contracts based on management estimates. 2 Projected revenue chart as prepared by Company management in the third quarter of 2021 and originally filed with the SEC on October 28, 2021. ($ in millions) Select Opportunity Sets Projected Revenue2 Extensive Opportunity Set Supported by Broad Array of Customers US DoD and IC Contracting Roadmap Research Agreements Initial Phase Multi-Year Recurring Revenue Subscriptions FY2025P FY2024P FY2022P FY2023P FY2026P US IC & Other USG Direct data sales in support of automated analytical solutions and services leveraging AI/ML Commercial & International Leverage global network of value-added resellers for commercial sales and to friendly foreign governments $500M+ Commercial Data-as-a-Service $900M+ Tactical ISR from Commercial Data $400M+ Foreign Allied Military Sales Select Target Customers and Opportunities1 US DoD Augment DoD assets with commercial constellation and direct downlink capabilities to the tactical edge |

| Financial Overview Gary Hobart Chief Financial Officer |

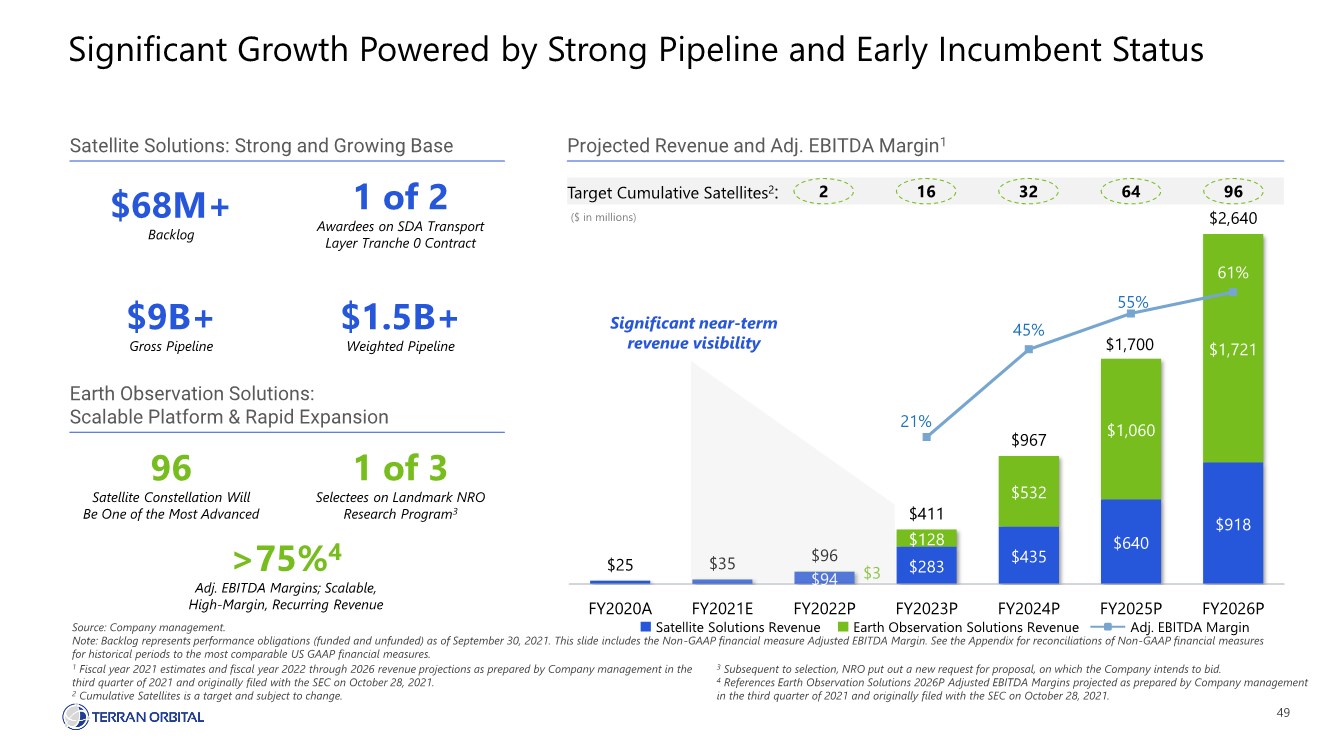

| 49 $94 $283 $435 $640 $918 $3 $128 $532 $1,060 $1,721 $25 $35 $96 $411 $967 $1,700 $2,640 21% 45% 55% 61% FY2020A FY2021E FY2022P FY2023P FY2024P FY2025P FY2026P Significant Growth Powered by Strong Pipeline and Early Incumbent Status Source: Company management. Note: Backlog represents performance obligations (funded and unfunded) as of September 30, 2021. This slide includes the Non-GAAP financial measure Adjusted EBITDA Margin. See the Appendix for reconciliations of Non-GAAP financial measures for historical periods to the most comparable US GAAP financial measures. Satellite Solutions: Strong and Growing Base $68M+ Backlog $9B+ Gross Pipeline $1.5B+ Weighted Pipeline 1 of 2 Awardees on SDA Transport Layer Tranche 0 Contract 96 Satellite Constellation Will Be One of the Most Advanced 1 of 3 Selectees on Landmark NRO Research Program3 >75%4 Adj. EBITDA Margins; Scalable, High-Margin, Recurring Revenue Earth Observation Solutions: Scalable Platform & Rapid Expansion Significant near-term revenue visibility Earth Observation Solutions Revenue Adj. EBITDA Margin Satellite Solutions Revenue Target Cumulative Satellites2: 2 96 64 32 16 ($ in millions) Projected Revenue and Adj. EBITDA Margin1 1 Fiscal year 2021 estimates and fiscal year 2022 through 2026 revenue projections as prepared by Company management in the third quarter of 2021 and originally filed with the SEC on October 28, 2021. 2 Cumulative Satellites is a target and subject to change. 3 Subsequent to selection, NRO put out a new request for proposal, on which the Company intends to bid. 4 References Earth Observation Solutions 2026P Adjusted EBITDA Margins projected as prepared by Company management in the third quarter of 2021 and originally filed with the SEC on October 28, 2021. |

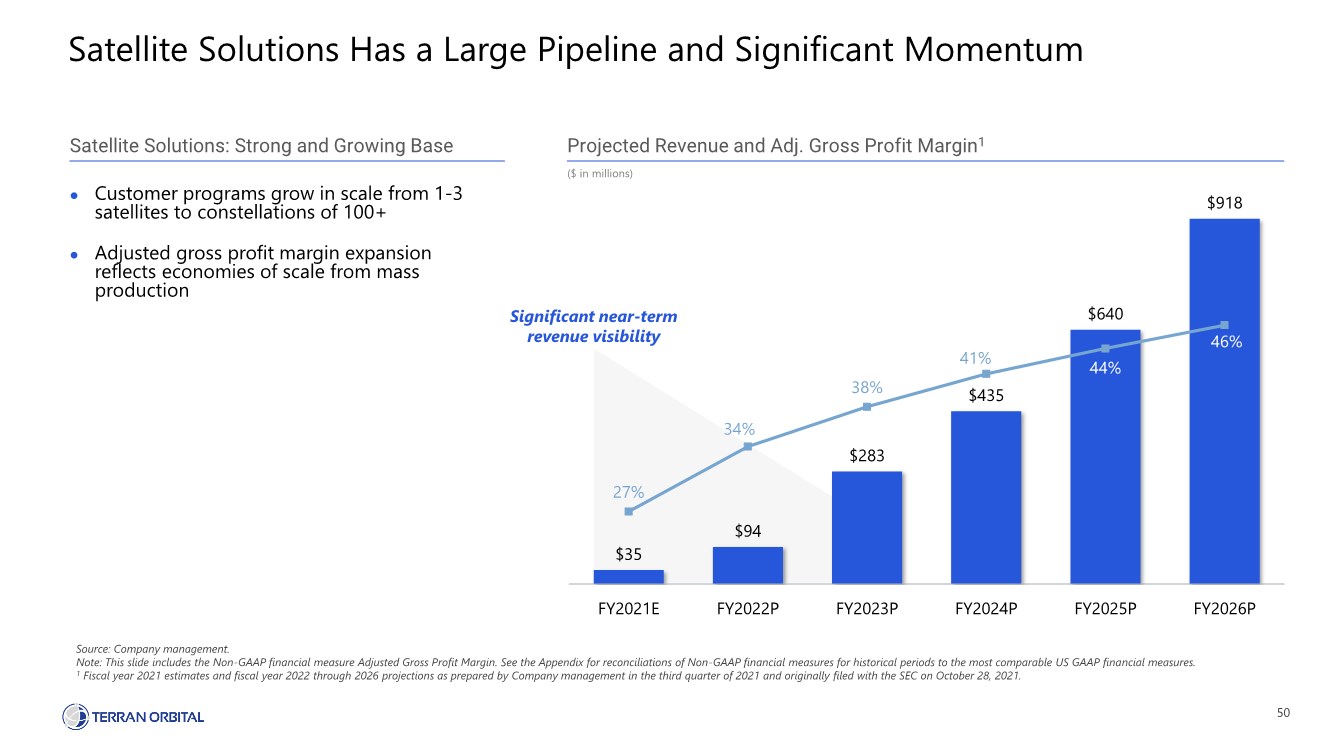

| 50 Satellite Solutions Has a Large Pipeline and Significant Momentum ($ in millions) $35 $94 $283 $435 $640 $918 27% 34% 38% 41% 44% 46% FY2021E FY2022P FY2023P FY2024P FY2025P FY2026P Satellite Solutions: Strong and Growing Base Projected Revenue and Adj. Gross Profit Margin1 Significant near-term revenue visibility ⚫ Customer programs grow in scale from 1-3 satellites to constellations of 100+ ⚫ Adjusted gross profit margin expansion reflects economies of scale from mass production Source: Company management. Note: This slide includes the Non-GAAP financial measure Adjusted Gross Profit Margin. See the Appendix for reconciliations of Non-GAAP financial measures for historical periods to the most comparable US GAAP financial measures. 1 Fiscal year 2021 estimates and fiscal year 2022 through 2026 projections as prepared by Company management in the third quarter of 2021 and originally filed with the SEC on October 28, 2021. |

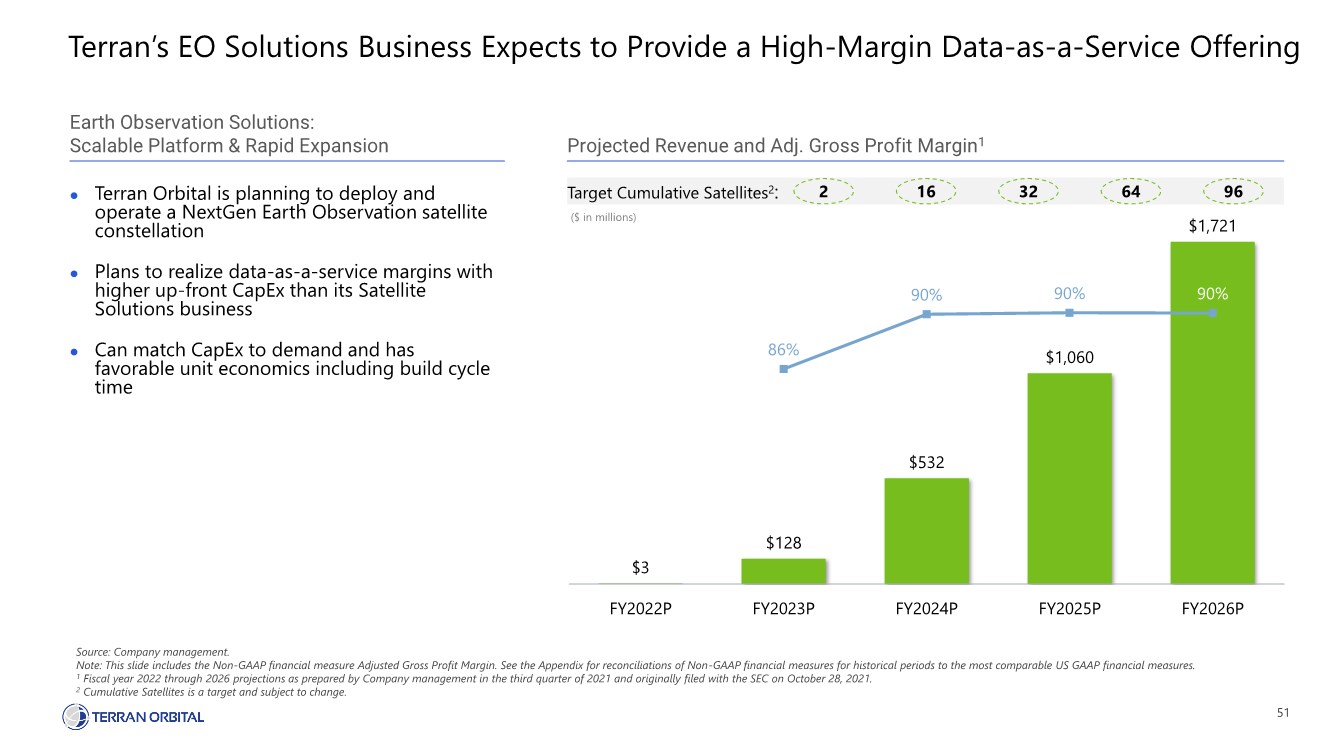

| 51 Terran’s EO Solutions Business Expects to Provide a High-Margin Data-as-a-Service Offering Source: Company management. Note: This slide includes the Non-GAAP financial measure Adjusted Gross Profit Margin. See the Appendix for reconciliations of Non-GAAP financial measures for historical periods to the most comparable US GAAP financial measures. 1 Fiscal year 2022 through 2026 projections as prepared by Company management in the third quarter of 2021 and originally filed with the SEC on October 28, 2021. 2 Cumulative Satellites is a target and subject to change. $3 $128 $532 $1,060 $1,721 86% 90% 90% 90% FY2022P FY2023P FY2024P FY2025P FY2026P Earth Observation Solutions: Scalable Platform & Rapid Expansion Projected Revenue and Adj. Gross Profit Margin1 ⚫ Terran Orbital is planning to deploy and operate a NextGen Earth Observation satellite constellation ⚫ Plans to realize data-as-a-service margins with higher up-front CapEx than its Satellite Solutions business ⚫ Can match CapEx to demand and has favorable unit economics including build cycle time Target Cumulative Satellites2: 2 96 64 32 16 ($ in millions) |

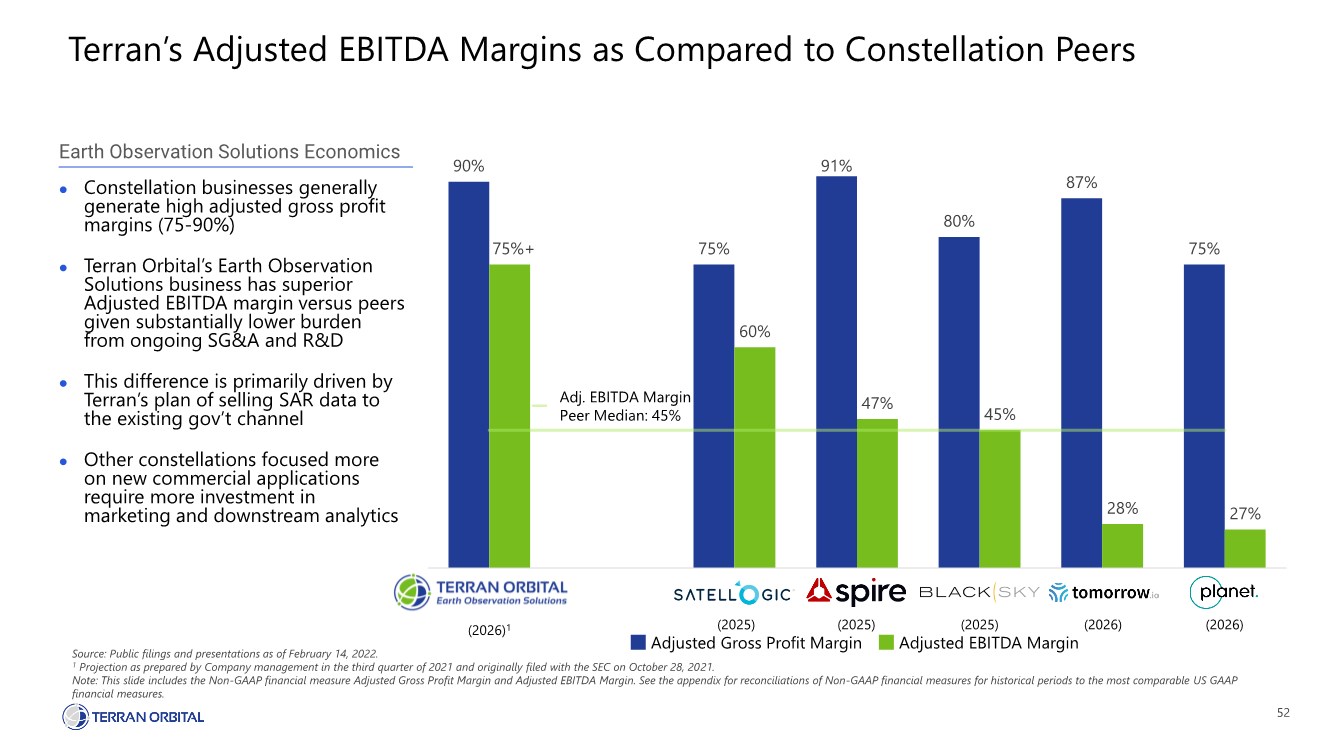

| 52 Terran’s Adjusted EBITDA Margins as Compared to Constellation Peers 90% 75% 91% 80% 87% 75% 75%+ 60% 47% 45% 28% 27% Earth Observation Solutions Economics ⚫ Constellation businesses generally generate high adjusted gross profit margins (75-90%) ⚫ Terran Orbital’s Earth Observation Solutions business has superior Adjusted EBITDA margin versus peers given substantially lower burden from ongoing SG&A and R&D ⚫ This difference is primarily driven by Terran’s plan of selling SAR data to the existing gov’t channel ⚫ Other constellations focused more on new commercial applications require more investment in marketing and downstream analytics Adjusted Gross Profit Margin Adjusted EBITDA Margin Source: Public filings and presentations as of February 14, 2022. 1 Projection as prepared by Company management in the third quarter of 2021 and originally filed with the SEC on October 28, 2021. Note: This slide includes the Non-GAAP financial measure Adjusted Gross Profit Margin and Adjusted EBITDA Margin. See the appendix for reconciliations of Non-GAAP financial measures for historical periods to the most comparable US GAAP financial measures. Adj. EBITDA Margin Peer Median: 45% (2025) (2025) (2025) (2026) (2026) (2026)1 |

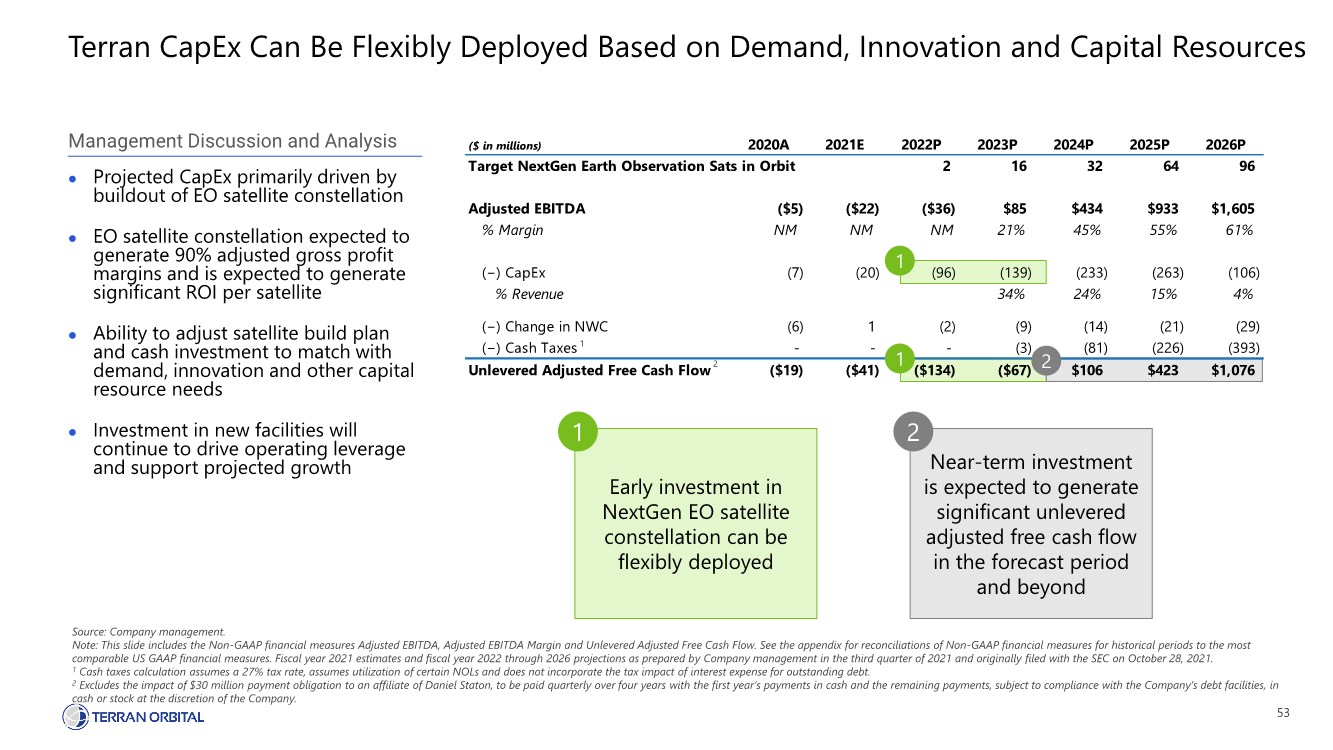

| 53 1 Terran CapEx Can Be Flexibly Deployed Based on Demand, Innovation and Capital Resources Source: Company management. Note: This slide includes the Non-GAAP financial measures Adjusted EBITDA, Adjusted EBITDA Margin and Unlevered Adjusted Free Cash Flow. See the appendix for reconciliations of Non-GAAP financial measures for historical periods to the most comparable US GAAP financial measures. Fiscal year 2021 estimates and fiscal year 2022 through 2026 projections as prepared by Company management in the third quarter of 2021 and originally filed with the SEC on October 28, 2021. 1 Cash taxes calculation assumes a 27% tax rate, assumes utilization of certain NOLs and does not incorporate the tax impact of interest expense for outstanding debt. 2 Excludes the impact of $30 million payment obligation to an affiliate of Daniel Staton, to be paid quarterly over four years with the first year’s payments in cash and the remaining payments, subject to compliance with the Company’s debt facilities, in cash or stock at the discretion of the Company. Management Discussion and Analysis ⚫ Projected CapEx primarily driven by buildout of EO satellite constellation ⚫ EO satellite constellation expected to generate 90% adjusted gross profit margins and is expected to generate significant ROI per satellite ⚫ Ability to adjust satellite build plan and cash investment to match with demand, innovation and other capital resource needs ⚫ Investment in new facilities will continue to drive operating leverage and support projected growth Near-term investment is expected to generate significant unlevered adjusted free cash flow in the forecast period and beyond Early investment in NextGen EO satellite constellation can be flexibly deployed 1 2 ($ in millions) 2020A 2021E 2022P 2023P 2024P 2025P 2026P Target NextGen Earth Observation Sats in Orbit 2 16 32 64 96 Adjusted EBITDA ($5) ($22) ($36) $85 $434 $933 $1,605 % Margin NM NM NM 21% 45% 55% 61% (−) CapEx (7) (20) (96) (139) (233) (263) (106) % Revenue 34% 24% 15% 4% (−) Change in NWC (6) 1 (2) (9) (14) (21) (29) (−) Cash Taxes ---(3) (81) (226) (393) Unlevered Adjusted Free Cash Flow ($19) ($41) ($134) ($67) $106 $423 $1,076 2 1 2 1 |

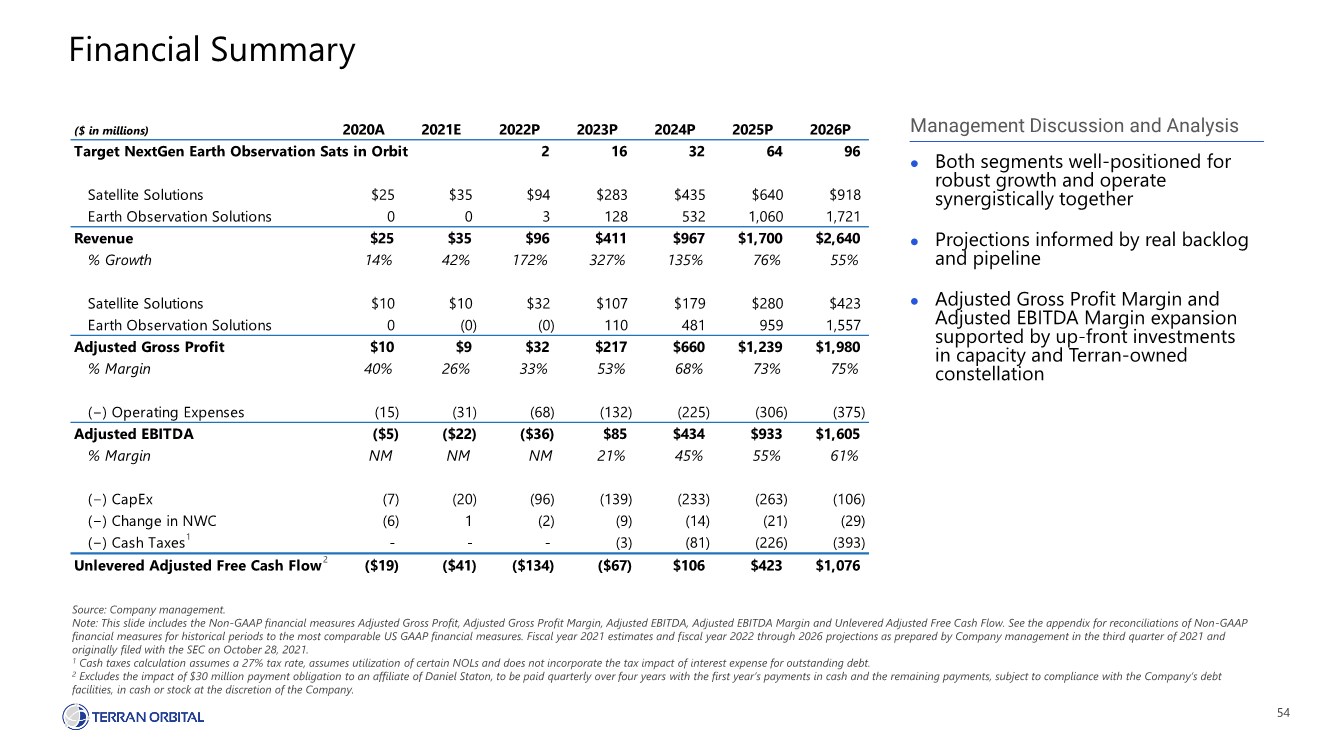

| 54 Financial Summary Source: Company management. Note: This slide includes the Non-GAAP financial measures Adjusted Gross Profit, Adjusted Gross Profit Margin, Adjusted EBITDA, Adjusted EBITDA Margin and Unlevered Adjusted Free Cash Flow. See the appendix for reconciliations of Non-GAAP financial measures for historical periods to the most comparable US GAAP financial measures. Fiscal year 2021 estimates and fiscal year 2022 through 2026 projections as prepared by Company management in the third quarter of 2021 and originally filed with the SEC on October 28, 2021. 1 Cash taxes calculation assumes a 27% tax rate, assumes utilization of certain NOLs and does not incorporate the tax impact of interest expense for outstanding debt. 2 Excludes the impact of $30 million payment obligation to an affiliate of Daniel Staton, to be paid quarterly over four years with the first year’s payments in cash and the remaining payments, subject to compliance with the Company’s debt facilities, in cash or stock at the discretion of the Company. Management Discussion and Analysis ⚫ Both segments well-positioned for robust growth and operate synergistically together ⚫ Projections informed by real backlog and pipeline ⚫ Adjusted Gross Profit Margin and Adjusted EBITDA Margin expansion supported by up-front investments in capacity and Terran-owned constellation ($ in millions) 2020A 2021E 2022P 2023P 2024P 2025P 2026P Target NextGen Earth Observation Sats in Orbit 2 16 32 64 96 Satellite Solutions $25 $35 $94 $283 $435 $640 $918 Earth Observation Solutions 0 0 3 128 532 1,060 1,721 Revenue $25 $35 $96 $411 $967 $1,700 $2,640 % Growth 14% 42% 172% 327% 135% 76% 55% Satellite Solutions $10 $10 $32 $107 $179 $280 $423 Earth Observation Solutions 0 (0) (0) 110 481 959 1,557 Adjusted Gross Profit $10 $9 $32 $217 $660 $1,239 $1,980 % Margin 40% 26% 33% 53% 68% 73% 75% (−) Operating Expenses (15) (31) (68) (132) (225) (306) (375) Adjusted EBITDA ($5) ($22) ($36) $85 $434 $933 $1,605 % Margin NM NM NM 21% 45% 55% 61% (−) CapEx (7) (20) (96) (139) (233) (263) (106) (−) Change in NWC (6) 1 (2) (9) (14) (21) (29) (−) Cash Taxes ---(3) (81) (226) (393) Unlevered Adjusted Free Cash Flow ($19) ($41) ($134) ($67) $106 $423 $1,076 2 1 |

| Q&A |

| Thank You |

| Appendix |

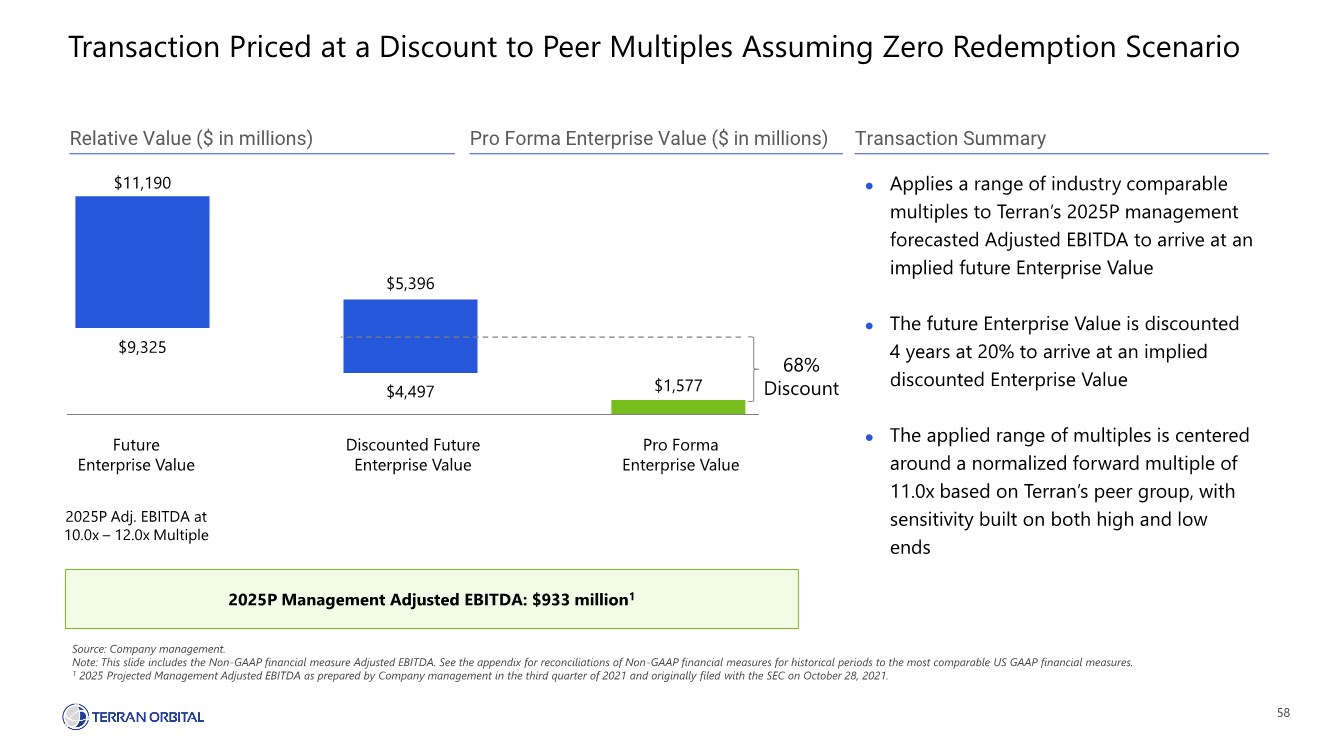

| 58 $9,325 $4,497 $1,577 $11,190 $5,396 Transaction Priced at a Discount to Peer Multiples Assuming Zero Redemption Scenario Source: Company management. Note: This slide includes the Non-GAAP financial measure Adjusted EBITDA. See the appendix for reconciliations of Non-GAAP financial measures for historical periods to the most comparable US GAAP financial measures. 1 2025 Projected Management Adjusted EBITDA as prepared by Company management in the third quarter of 2021 and originally filed with the SEC on October 28, 2021. Relative Value ($ in millions) Transaction Summary ⚫ Applies a range of industry comparable multiples to Terran’s 2025P management forecasted Adjusted EBITDA to arrive at an implied future Enterprise Value ⚫ The future Enterprise Value is discounted 4 years at 20% to arrive at an implied discounted Enterprise Value ⚫ The applied range of multiples is centered around a normalized forward multiple of 11.0x based on Terran’s peer group, with sensitivity built on both high and low ends 68% Discount Pro Forma Enterprise Value ($ in millions) 2025P Management Adjusted EBITDA: $933 million1 Pro Forma Enterprise Value Discounted Future Enterprise Value Future Enterprise Value 2025P Adj. EBITDA at 10.0x – 12.0x Multiple |

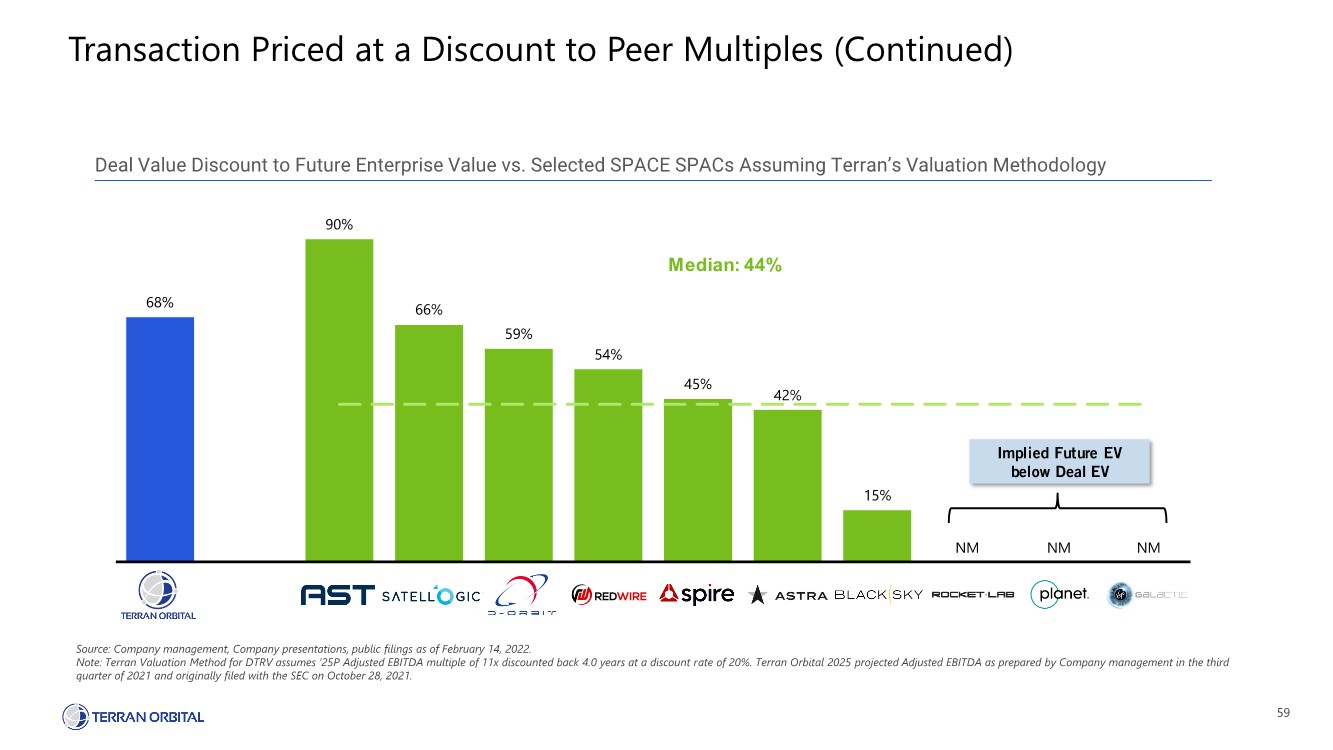

| 59 Transaction Priced at a Discount to Peer Multiples (Continued) Source: Company management, Company presentations, public filings as of February 14, 2022. Note: Terran Valuation Method for DTRV assumes ‘25P Adjusted EBITDA multiple of 11x discounted back 4.0 years at a discount rate of 20%. Terran Orbital 2025 projected Adjusted EBITDA as prepared by Company management in the third quarter of 2021 and originally filed with the SEC on October 28, 2021. Deal Value Discount to Future Enterprise Value vs. Selected SPACE SPACs Assuming Terran’s Valuation Methodology 68% 90% 66% 59% 54% 45% 42% 15% NM NM NM Implied Future EV below Deal EV Median: 44% |

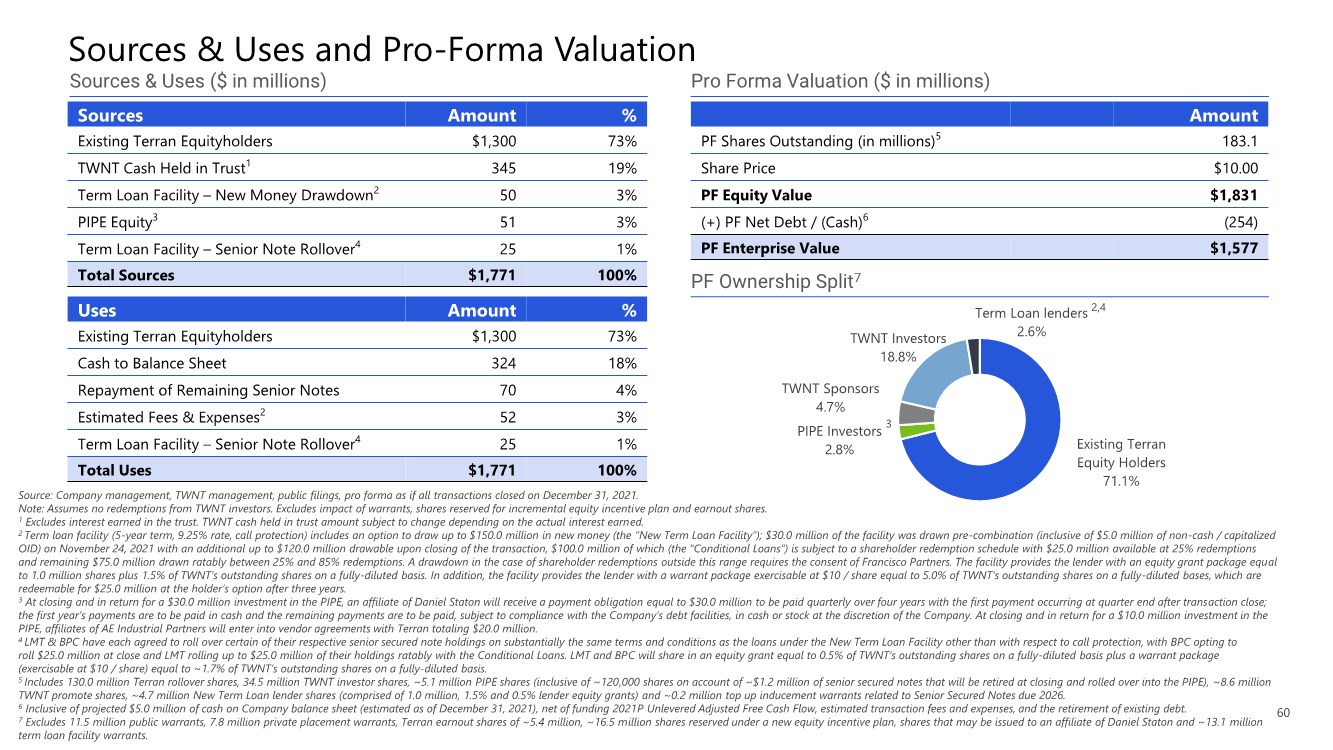

| 60 Sources & Uses and Pro-Forma Valuation Sources Amount % Existing Terran Equityholders $1,300 73% TWNT Cash Held in Trust1 345 19% Term Loan Facility – New Money Drawdown2 50 3% PIPE Equity3 51 3% Term Loan Facility – Senior Note Rollover4 25 1% Total Sources $1,771 100% Uses Amount % Existing Terran Equityholders $1,300 73% Cash to Balance Sheet 324 18% Repayment of Remaining Senior Notes 70 4% Estimated Fees & Expenses2 52 3% Term Loan Facility – Senior Note Rollover4 25 1% Total Uses $1,771 100% Amount PF Shares Outstanding (in millions)5 183.1 Share Price $10.00 PF Equity Value $1,831 (+) PF Net Debt / (Cash)6 (254) PF Enterprise Value $1,577 Sources & Uses ($ in millions) Pro Forma Valuation ($ in millions) PF Ownership Split7 Existing Terran Equity Holders 71.1% PIPE Investors 2.8% TWNT Sponsors 4.7% TWNT Investors 18.8% Term Loan lenders 2.6% 2,4 3 Source: Company management, TWNT management, public filings, pro forma as if all transactions closed on December 31, 2021. Note: Assumes no redemptions from TWNT investors. Excludes impact of warrants, shares reserved for incremental equity incentive plan and earnout shares. 1 Excludes interest earned in the trust. TWNT cash held in trust amount subject to change depending on the actual interest earned. 2 Term loan facility (5-year term, 9.25% rate, call protection) includes an option to draw up to $150.0 million in new money (the “New Term Loan Facility”); $30.0 million of the facility was drawn pre-combination (inclusive of $5.0 million of non-cash / capitalized OID) on November 24, 2021 with an additional up to $120.0 million drawable upon closing of the transaction, $100.0 million of which (the “Conditional Loans”) is subject to a shareholder redemption schedule with $25.0 million available at 25% redemptions and remaining $75.0 million drawn ratably between 25% and 85% redemptions. A drawdown in the case of shareholder redemptions outside this range requires the consent of Francisco Partners. The facility provides the lender with an equity grant package equal to 1.0 million shares plus 1.5% of TWNT’s outstanding shares on a fully-diluted basis. In addition, the facility provides the lender with a warrant package exercisable at $10 / share equal to 5.0% of TWNT’s outstanding shares on a fully-diluted bases, which are redeemable for $25.0 million at the holder’s option after three years. 3 At closing and in return for a $30.0 million investment in the PIPE, an affiliate of Daniel Staton will receive a payment obligation equal to $30.0 million to be paid quarterly over four years with the first payment occurring at quarter end after transaction close; the first year’s payments are to be paid in cash and the remaining payments are to be paid, subject to compliance with the Company’s debt facilities, in cash or stock at the discretion of the Company. At closing and in return for a $10.0 million investment in the PIPE, affiliates of AE Industrial Partners will enter into vendor agreements with Terran totaling $20.0 million. 4 LMT & BPC have each agreed to roll over certain of their respective senior secured note holdings on substantially the same terms and conditions as the loans under the New Term Loan Facility other than with respect to call protection, with BPC opting to roll $25.0 million at close and LMT rolling up to $25.0 million of their holdings ratably with the Conditional Loans. LMT and BPC will share in an equity grant equal to 0.5% of TWNT’s outstanding shares on a fully-diluted basis plus a warrant package (exercisable at $10 / share) equal to ~1.7% of TWNT’s outstanding shares on a fully-diluted basis. 5 Includes 130.0 million Terran rollover shares, 34.5 million TWNT investor shares, ~5.1 million PIPE shares (inclusive of ~120,000 shares on account of ~$1.2 million of senior secured notes that will be retired at closing and rolled over into the PIPE), ~8.6 million TWNT promote shares, ~4.7 million New Term Loan lender shares (comprised of 1.0 million, 1.5% and 0.5% lender equity grants) and ~0.2 million top up inducement warrants related to Senior Secured Notes due 2026. 6 Inclusive of projected $5.0 million of cash on Company balance sheet (estimated as of December 31, 2021), net of funding 2021P Unlevered Adjusted Free Cash Flow, estimated transaction fees and expenses, and the retirement of existing debt. 7 Excludes 11.5 million public warrants, 7.8 million private placement warrants, Terran earnout shares of ~5.4 million, ~16.5 million shares reserved under a new equity incentive plan, shares that may be issued to an affiliate of Daniel Staton and ~13.1 million term loan facility warrants. |

| 61 World Class Management Team Proven Track-Record of Designing, Executing and Operating in Space Marc Bell Co-Founder and Chief Executive Officer ⚫ Founder of Globix Corporation: The Global Internet Exchange, an Internet Infrastructure company that has laid over 28,000 miles of fiber and developed over 1 million square feet of Data Center Space ⚫ Took public a $250 million Special Purpose Acquisition Company (“SPAC”), which acquired startup Armour Residential REIT (NYSE: ARR) ⚫ Co-founder of Javelin Mortgage Investment Corp., acquired by Armour in 2016 Tony Previte Co-Founder and Chief Strategy Officer ⚫ Previously served as Terran Orbital’s President & Chief Executive Officer from 2014 to 2021 ⚫ Served as CEO of Starsmith, an investment holding company focused on acquiring controlling interests in scientific and technological-based companies from 2003 to 2008 ⚫ Served as the CTO and COO at Globix Corporation from 1998 to 2003 ⚫ Served as a Vice President of EMCOR from 1986 to 1998 Marco Villa Executive Vice President & Chief Revenue Officer ⚫ Previously served as Director of Mission Operations at SpaceX, where he developed and managed the Dragon Spacecraft Operations and helped secure $2.5B in contracts including the Commercial Crew Contract ⚫ Founder / Partner of mv2space, a business development, strategy formulation and support services consultancy ⚫ Aerospace and high technology advisor for Floyd Associates, a leading consulting services firm with expertise in corporate finance, business strategy and mergers and acquisitions Gary Hobart Chief Financial Officer and Executive Vice President ⚫ 30+ years of experience in investment management, banking, corporate finance and law, as both a principal investor as well as in an operational capacity over finance and accounting activities ⚫ Previously served as Managing Director of Beach Point Capital Management, where he focused on private debt and special situation investing ⚫ Prior to Beach Point, was an Investment Officer in the leveraged finance group of Trust Company of the West and a Vice President at Wasserstein Perella Source: Company management. |

| 62 World Class Management Team (Continued) Proven Track-Record of Designing, Executing and Operating in Space Source: Company management. Maj Gen Roger Teague, USAF (Ret.) President, Defense and Intelligence Systems ⚫ Previously served as Vice President, Space Intelligence and Missile Defense for Boeing ⚫ In 2017, completed 31 years of distinguished service in the United States Air Force, retiring in the rank of Major General ⚫ Led several crucial US space programs, including service as Director, Space Programs, Assistant Secretary for Acquisition during last duty assignment ⚫ Currently serves as National Director for the Air Force Association and as a Trustee for United Through Reading Lt Gen Dave Mann, USA (Ret.) Vice President, Strategy, Army Systems & Defense Programs ⚫ Previously served as independent consultant for various defense companies and government organizations ⚫ In 2017, completed more than 35 years of service in the United States Army, retiring in the rank of Lieutenant General ⚫ In his last assignment, served as the Commanding General for the US Army’s Space and Missile Defense Command/Army Forces Strategic Command Rear Adm Christian “Boris” Becker, USN (Ret.) President, Satellite Solutions ⚫ Completed more than 33 years of distinguished service in the United States Navy ⚫ Most recently commanded the US Navy’s Naval Information Warfare Systems Command (“NAVWAR”) ⚫ Served in leadership roles within Naval Air Systems Command (“NAVAIR”), Space & Naval Warfare Systems Command (“SPAWAR”), and the National Reconnaissance Office (“NRO”) |

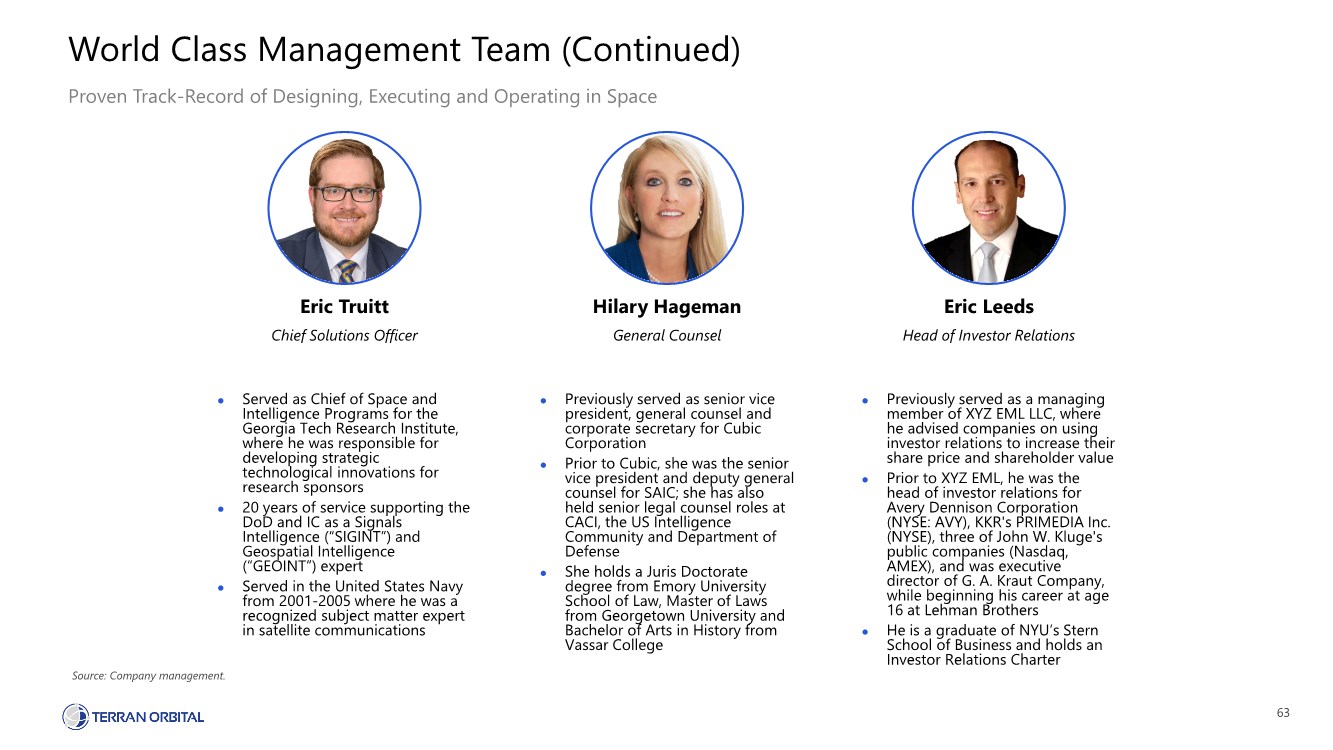

| 63 Hilary Hageman General Counsel ⚫ Previously served as senior vice president, general counsel and corporate secretary for Cubic Corporation ⚫ Prior to Cubic, she was the senior vice president and deputy general counsel for SAIC; she has also held senior legal counsel roles at CACI, the US Intelligence Community and Department of Defense ⚫ She holds a Juris Doctorate degree from Emory University School of Law, Master of Laws from Georgetown University and Bachelor of Arts in History from Vassar College Eric Truitt Chief Solutions Officer ⚫ Served as Chief of Space and Intelligence Programs for the Georgia Tech Research Institute, where he was responsible for developing strategic technological innovations for research sponsors ⚫ 20 years of service supporting the DoD and IC as a Signals Intelligence (“SIGINT”) and Geospatial Intelligence (“GEOINT”) expert ⚫ Served in the United States Navy from 2001-2005 where he was a recognized subject matter expert in satellite communications World Class Management Team (Continued) Proven Track-Record of Designing, Executing and Operating in Space Source: Company management. Eric Leeds Head of Investor Relations ⚫ Previously served as a managing member of XYZ EML LLC, where he advised companies on using investor relations to increase their share price and shareholder value ⚫ Prior to XYZ EML, he was the head of investor relations for Avery Dennison Corporation (NYSE: AVY), KKR's PRIMEDIA Inc. (NYSE), three of John W. Kluge's public companies (Nasdaq, AMEX), and was executive director of G. A. Kraut Company, while beginning his career at age 16 at Lehman Brothers ⚫ He is a graduate of NYU’s Stern School of Business and holds an Investor Relations Charter |

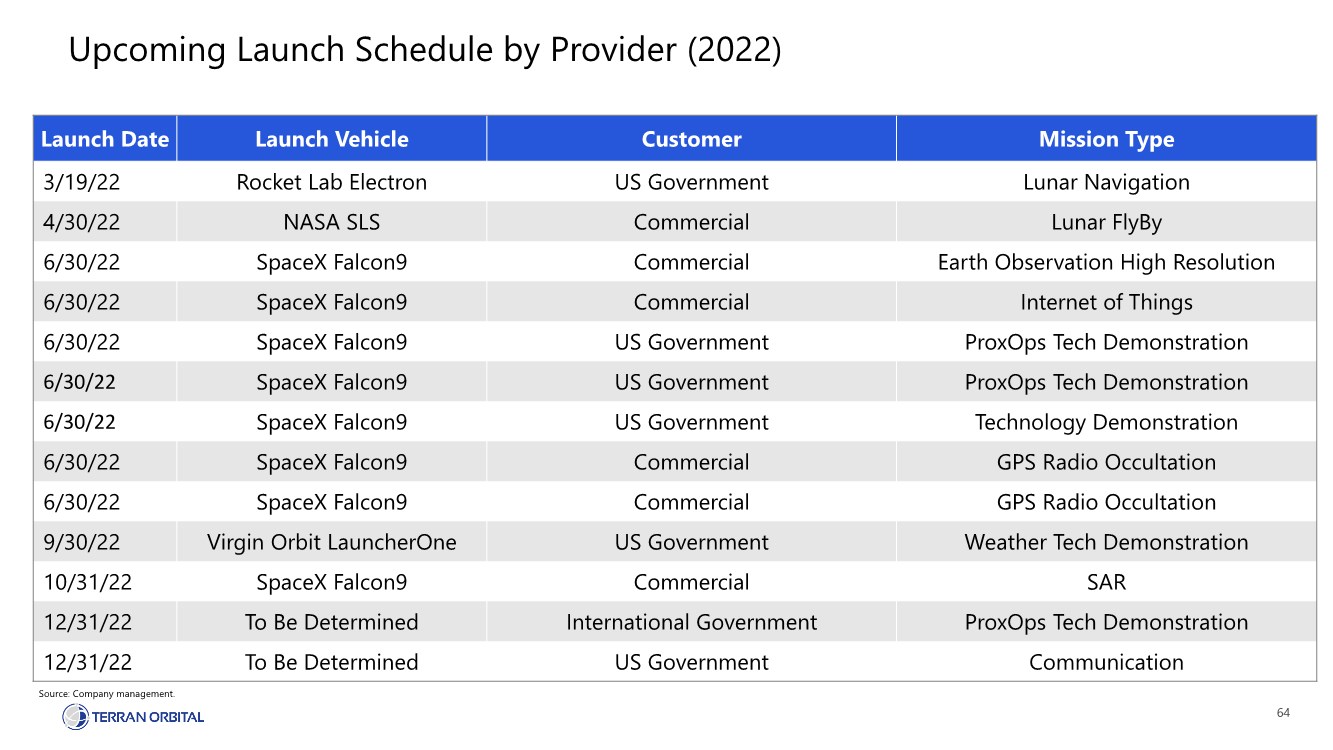

| 64 Upcoming Launch Schedule by Provider (2022) Source: Company management. Launch Date Launch Vehicle Customer Mission Type 3/19/22 Rocket Lab Electron US Government Lunar Navigation 4/30/22 NASA SLS Commercial Lunar FlyBy 6/30/22 SpaceX Falcon9 Commercial Earth Observation High Resolution 6/30/22 SpaceX Falcon9 Commercial Internet of Things 6/30/22 SpaceX Falcon9 US Government ProxOps Tech Demonstration 6/30/22 SpaceX Falcon9 US Government ProxOps Tech Demonstration 6/30/22 SpaceX Falcon9 US Government Technology Demonstration 6/30/22 SpaceX Falcon9 Commercial GPS Radio Occultation 6/30/22 SpaceX Falcon9 Commercial GPS Radio Occultation 9/30/22 Virgin Orbit LauncherOne US Government Weather Tech Demonstration 10/31/22 SpaceX Falcon9 Commercial SAR 12/31/22 To Be Determined International Government ProxOps Tech Demonstration 12/31/22 To Be Determined US Government Communication |

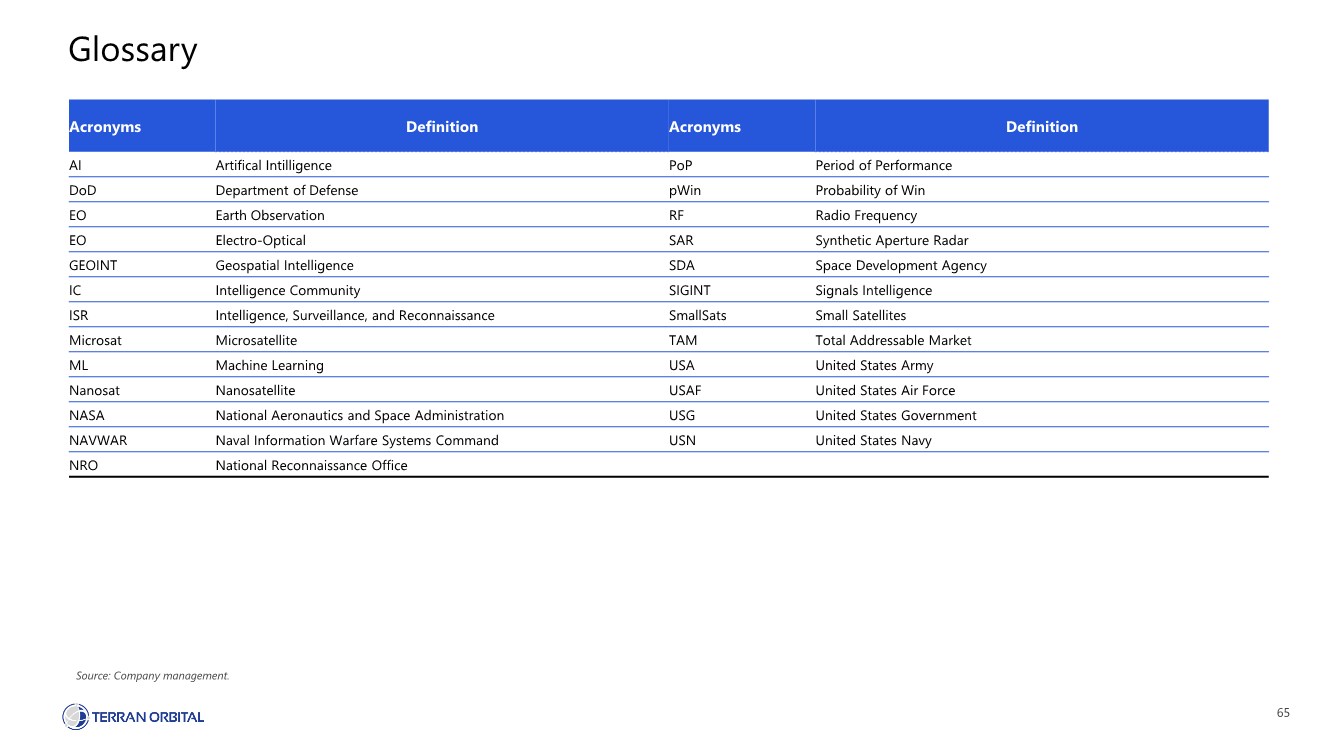

| 65 Glossary Acronyms Definition Acronyms Definition AI Artifical Intilligence PoP Period of Performance DoD Department of Defense pWin Probability of Win EO Earth Observation RF Radio Frequency EO Electro-Optical SAR Synthetic Aperture Radar GEOINT Geospatial Intelligence SDA Space Development Agency IC Intelligence Community SIGINT Signals Intelligence ISR Intelligence, Surveillance, and Reconnaissance SmallSats Small Satellites Microsat Microsatellite TAM Total Addressable Market ML Machine Learning USA United States Army Nanosat Nanosatellite USAF United States Air Force NASA National Aeronautics and Space Administration USG United States Government NAVWAR Naval Information Warfare Systems Command USN United States Navy NRO National Reconnaissance Office Source: Company management. |

| 66 Disclaimer This Investor Presentation (this “Presentation”) is being provided for informational purposes in connection with the analyst and investor days to be held on February 16 and 17, 2022 in connection with the proposed business combination (the “Business Combination”) between Terran Orbital Corporation (the “Company”) and Tailwind Two Acquisition Corp. (“Tailwind”). The information in this Presentation discusses trends and markets that the leadership team of the Company believes will impact the development and success of the Company based on its current understanding of the industry. Such information has not been independently verified by Tailwind. None of the Company, Tailwind, their respective affiliates or their respective employees, directors, officers, contractors, advisors, members, successors, representatives or agents makes any representation or warranty as to the accuracy, reasonableness or completeness of the information contained in this Presentation, and shall have no liability for any representations or warranties (expressed or implied) contained in, or for any omissions from or errors in, this Presentation or any other written or oral communications transmitted to the recipient in the course of its evaluation of the Company, Tailwind or the Business Combination. Only those representations and warranties as may be contained in definitive written agreements relating to the Business Combination shall have any legal effect. The information in this Presentation speaks only as of the date of this Presentation and is subject to change. The Company and Tailwind are under no obligation to update, amend or supplement this Presentation or any information contained herein. This Presentation includes certain forward-looking statements, estimates, and projections provided by the Company that reflect management’s views regarding the anticipated future financial and operating performance of the Company. Forward-looking statements are statements that are not historical, including statements regarding operational and financial plans, terms and performance of the Company and other projections or predictions of the future. Forward looking statements are typically identified by such words as “project,” “believe,” “expect,” “anticipate,” “intend,” “estimate,” “may,” “will,” “should,” and “could” and similar expressions. Such statements, estimates, and projections reflect numerous assumptions concerning anticipated results. Forward- looking statements in this Presentation may include, for example; statements about the Company’s industry and market sizes; future opportunities; expectations and projections concerning future financial and operational performance and results of the Company and the Business Combination, including items such as the implied enterprise value, ownership structure, the amount of redemption requests made by Tailwind’s shareholders, the ability of Tailwind to issue equity or equity-linked instruments in connection with the Business Combination or in the future, the likelihood and ability of the parties to successfully consummate the Business Combination, and those factors set forth on the next page of this Presentation under the heading “Risk Factors” and those factors set forth in the sections entitled “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements; Market Ranking and Other Industry Data” in Tailwind's definitive proxy statement referred to below and in subsequent filings with the Securities and Exchange Commission (“SEC”) filed by Tailwind. As these assumptions may or may not prove to be correct and there are numerous factors which will affect the Company’s actual results (many of which are beyond the Company’s control), there can be no assurances that any projected results are attainable or will be realized. The Company and Tailwind disclaim any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events, or otherwise. The Company’s actual results may differ materially from those set forth in this Presentation. Accordingly, no representations are made as to the accuracy, reasonableness or completeness of such statements, estimates, or projections. This Presentation includes certain non-GAAP financial measures. For more information with respect to such measures, please refer to Appendix slide covering Non-GAAP Financial Measures. This Presentation contains financial forecasts with respect to the Company's projected financial results and operating data, including target Earth Observation satellites in orbit and related metrics, revenue, gross profit, SG&A, research and development, Adjusted EBITDA, Adjusted EBITDA Margin, Adjusted Gross Profit, Adjusted Gross Profit Margin, capital expenditures, net working capital, cash taxes, Unlevered Adjusted Free Cash Flow, total enterprise value, and backlog for the periods ending in December 31, 2021, 2022, 2023, 2024, 2025, and 2026, as prepared by Company management in the third quarter of 2021 and originally filed with the SEC on October 28, 2021. The forecasts do not take into account any circumstances or events occurring after they were prepared. Accordingly, they should not be looked upon as “guidance” of any sort. The Company will not refer back to these forecasts in its future periodic reports filed under the Securities Exchange Act of 1934. Neither the Company's independent auditors, nor Tailwind’s independent registered public accounting firm, has audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this Presentation, and accordingly, neither of them expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this Presentation. These projections should not be relied upon as being necessarily indicative of future results. The assumptions and estimates underlying the prospective financial information are inherently uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the prospective financial information, including those references under "forward-looking statements" above. Accordingly, there can be no assurance that the prospective results are indicative of the Company’s future performance or that actual results will not differ materially from those presented in the prospective financial information. Inclusion of the prospective financial information in this Presentation should not be regarded as a representation by any person that the results contained in such prospective financial information will be achieved. This Presentation and any oral statements made in connection with this Presentation shall not constitute an offer, nor a solicitation of an offer, of the sale or purchase of any securities, nor shall any securities of the Company or Tailwind be offered or sold, in any jurisdiction in which such an offer, solicitation or sale would be unlawful. Neither the SEC nor any state securities commission has approved or disapproved of the transactions contemplated hereby or determined if this Presentation is truthful or complete. Any representation to the contrary is a criminal offense. Nothing in this Presentation constitutes investment, tax or legal advice or a recommendation regarding any securities. You should consult your own counsel and tax and financial advisors as to legal and related matters concerning the matters described herein, must make your own decisions and perform your own independent investment and analysis of the Business Combination, and, by accepting this Presentation, you confirm that you are not relying upon the information contained herein to make any decision. Certain information contained herein has been derived from sources prepared by third parties. While such information is believed to be reliable for the purposes used herein, neither the Company nor Tailwind makes any representation or warranty with respect to the accuracy of such information. In this Presentation, Tailwind and the Company rely on and refer to certain information and statistics obtained from third-party sources including reports by market research firms. Neither Tailwind nor the Company has independently verified the accuracy or completeness of any such third-party information. You are cautioned not to give undue weight to such industry and market data. Any and all trademarks and trade names referred to in this presentation are the property of their respective owners. In connection with the Business Combination, Tailwind has filed, and the SEC has declared effective on February 14, 2022, a registration statement on Form S-4 containing a definitive proxy statement/prospectus. Tailwind has mailed the definitive proxy statement/prospectus and other documents relating to the Business Combination to its shareholders as of a record date of February 4, 2022. This Presentation does not contain all the information that should be considered concerning the Business Combination and is not intended to form the basis of any investment decision or any other decision in respect of the Business Combination. Tailwind’s shareholders and other interested persons are advised to read the definitive proxy statement/prospectus as it contains important information about the Company, Tailwind and the Business Combination. Shareholders are also able to obtain copies of the definitive proxy statement/prospectus and other documents filed with the SEC, without charge, at the SEC's website sec.gov. Tailwind and its directors and executive officers may be deemed participants in the solicitation of proxies from Tailwind's shareholders with respect to the Business Combination. The Company and its directors and executive officers may also be deemed to be participants in the solicitation of proxies from Tailwind’s shareholders in connection with the Business Combination. A list of the names of those directors and executive officers of Tailwind and the Company and a description of their interests in the Business Combination is contained in the definitive proxy statement/prospectus filed with the SEC. |

| 67 Risk Factors The risks presented below are certain of the general risks related to the Company’s business, industry and ownership structure and are not exhaustive. The list below is qualified in its entirety by disclosures contained in the definitive proxy statement / prospectus filed by Tailwind with the SEC and in subsequent filings. These risks speak only as of the date of this presentation and neither Tailwind nor the Company makes any commitment to update such disclosure. ⚫ Upon consummation of the Business Combination, the combined company will have a substantial amount of indebtedness and payment obligations that could affect operations and financial condition and prevent it from fulfilling its obligations under its indebtedness. ⚫ The Company may not be able to convert its orders in backlog or the sales opportunities represented in its pipeline into revenue. ⚫ The Company is an early-stage company with a history of losses and may not achieve or maintain profitability. ⚫ The Company’s historical financial results and its unaudited pro forma condensed combined financial information may not be indicative of what its actual financial position or results of operations would have been. ⚫ The Company has a limited operating history and operates in a rapidly evolving industry, which makes it difficult to evaluate its business and future prospects and increases the risk of your investment. ⚫ The Company will incur significant expenses and capital expenditures in the future to execute its business plan and expand satellite solutions and develop its mission and data solutions within its Earth Observation Solutions, in particular the development of its NextGen Earth Observation constellation, and it may be not be able to adequately control its expenses. ⚫ The Company relies indirectly on contracts with U.S. government entities for a substantial portion of its revenues, and its business is concentrated in a small number of primary contracts. The loss or reduction in scope of any one of its primary contracts would materially reduce its revenue. ⚫ Government customers subject the Company to risks including early termination, audits, investigations, sanctions and penalties. ⚫ Lockheed Martin Corporation (“Lockheed Martin”) accounts for a substantial portion of the Company’s revenue. If Lockheed Martin changes its business strategy or reduces its demand for the Company’s products and services, the Company’s business, prospects, operating results and financial condition could be adversely effected. ⚫ Following the completion of the Business Combination, including the PIPE Financing and the Debt Financings, the Company may still require substantial additional funding to finance its operations, but adequate additional financing may not be available when it needs it, on acceptable terms or at all. If the Company cannot raise additional funds when needed, its operations and prospects could be negatively affected. ⚫ The Company’s Earth Observation Solutions’ satellite constellation, including the SAR technology and satellite bus size, are under design and development, have not been built or launched by it before and may not be completed on time or at all, may not work properly, and the costs associated with it may be greater than expected. There is technology, development and cost risk associated with the Company’s Earth Observation Solutions’ satellites that if not successfully managed will have a significant impact on the Company’s ability to successfully deploy and commercialize its Earth Observation Solutions’ business. ⚫ Rapid and significant technological changes or advancements in competitors’ offerings could render the Company’s NextGen Earth Observation constellation and its Satellite Solutions offerings obsolete and impair its ability to compete. ⚫ The Company is highly dependent on the services of Marc Bell, its co-founder and Chief Executive Officer, and if the Company is unable to retain Mr. Bell, as well as attract and retain key employees, qualified management, technical and engineering personnel, its ability to compete could be harmed. ⚫ A failure to successfully finance, open and operate the Space Florida Facility could harm the Company’s business, financial condition and results of operations. This expansion may not be achieved on time or within the Company’s projected budget and may otherwise not provide the capability that it seeks. ⚫ If the Company fails to manage its future growth effectively, its business, prospects, operating results and financial condition may be materially adversely effected. ⚫ Rapid and significant technological changes or advancements in competitors’ offerings could render the NextGen Earth Observation constellation and the Company’s Satellite Solutions offerings obsolete and impair its ability to compete. ⚫ The Company depends on its ability to generate a sustainable order rate for the satellite manufacturing operations and develop new technologies to meet the needs of its customers or potential new customers. ⚫ The Company relies on third parties for a supply of equipment, satellite and other components, including semiconductor chip components, and services which creates risks to its operations. In addition, any future delays in delivery could adversely affect its financial performance and future prospects. ⚫ The Company and its suppliers rely on complex systems and components, which involves a significant degree of risk and uncertainty in terms of operational performance and costs. ⚫ The Company may be negatively affected by global economic conditions or geopolitical factors. ⚫ The ongoing COVID-19 pandemic and future pandemics and health crises may disrupt the Company’s operations and affect its ability to successfully complete the research and development of its NextGen Earth Observation constellation on a timely basis. ⚫ Satellites are subject to construction and launch delays, launch failures, damage or destruction during launch, the occurrence of which can materially and adversely affect the Company’s operations. The Company may not be able to secure the launch of its satellites successfully or in a timely manner. Loss of a satellite during launch could delay or impair the Company’s ability to offer its services or reduce its expected potential revenues, and launch insurance, even if it is available, will not fully cover this risk. ⚫ The Company is dependent on third-party launch vehicles to launch its satellites into space and any delay could have an adverse impact. Price increases from these third-party launch providers could negatively impact the Company’s business model and profitability. ⚫ The Company’s products could fail to perform or could perform at reduced levels of service because of technological malfunctions or deficiencies, regulatory compliance issues, or events outside of its control, which would harm its business and reputation. ⚫ The Company’s satellites have a limited life and may fail prematurely, which would materially and adversely affect its business, prospects and potential profitability. ⚫ The Company’s business may be adversely affected if it is unable to protect its intellectual property from unauthorized use by third parties. ⚫ Because the Company’s satellites are complex and are deployed in complex environments, its satellites may have defects that are discovered only after full deployment to space, which could seriously harm the Company’s business. The Company’s customized hardware and software may be difficult and expensive to service, upgrade or replace. ⚫ Security problems with the Company’s networks, data processing systems, software products, and those systems or services of its third-party providers may be vulnerable to security risks, could cause increased cyber-security protection costs and general service costs, harm its reputation, and result in liability and increased expense for litigation, regulatory fines and diversion of management time. ⚫ Natural disasters could disrupt the Company’s business, including its vehicle launch schedule. ⚫ The Company’s satellites may collide with space debris or another spacecraft, which could adversely affect its performance of any satellites it builds and places in orbit, including those satellites in its NextGen Earth Observation constellation. ⚫ The Company’s business involves significant risks and uncertainties that may not be covered by insurance. ⚫ The Company’s business is subject to extensive government regulation, which mandates how it may operate its business, may reduce or eliminate its business, and may increase its business costs and prevent its expansion into new markets. ⚫ The Company may become involved in litigation, including securities class action litigation relating to the proposed business combination, that may materially adversely affect it. ⚫ The Company identified material weaknesses in its internal control over financial reporting as of December 31, 2020 and, as a result, the Company has determined that its disclosure controls and procedures were not effective as of December 31, 2020. If the Company is unable to remediate these material weaknesses, or if it identifies additional material weaknesses in the future or otherwise fails to maintain effective internal control over financial reporting, it may not be able to accurately or timely report its financial condition or results or operations, which may adversely affect its business, stock price and operating results. ⚫ The Company has not yet applied for, and may not receive, certain regulatory approvals that are necessary to its business plan. The Company will rely on certain regulatory approvals to manufacture, launch, export, operate and transmit controls and data, the failure to obtain these approvals may impact its ability to provide certain goods and services. Foreign Ownership, Control or Influence could negatively impact its ability to obtain certain regulatory approvals. ⚫ Future sales, or the perception of future sales, by the combined company or its stockholders in the public market following the Business Combination could cause the market price for the combined company’s securities to decline. |

| 68 Non-GAAP Financial Measures This Presentation includes non-GAAP financial measures, such as Adjusted Gross Profit, Adjusted Gross Profit Margin, Adjusted EBITDA, Adjusted EBITDA Margin, Adjusted Free Cash Flow and Unlevered Adjusted Free Cash Flow, that have not been prepared in accordance with United States generally accepted accounting principles (“GAAP”). The non-GAAP measures in this Presentation may be different from non-GAAP calculations made by other companies. The recipient should be aware that the presentation of these measures may not be comparable to similarly-titled measures used by other companies. These measures may exclude items that are significant in understanding and assessing the Company’s financial results. Therefore, these measures should not be considered in isolation or as an alternative to net income or other measures of financial performance or liquidity under GAAP. Please refer to the last slide of this Presentation for a reconciliation of such non-GAAP measures to their most directly comparable measures presented in accordance with GAAP. The Company is not providing a reconciliation of Adjusted Gross Profit, Adjusted Gross Profit Margin, Adjusted EBITDA, Adjusted EBITDA Margin, Adjusted Free Cash Flow and Unlevered Adjusted Free Cash Flow on a forward-looking basis to the most directly comparable measure prepared in accordance with GAAP because the Company is unable to provide this reconciliation without unreasonable effort due to the uncertainty and inherent difficulty of predicting the occurrence, the financial impact, and the periods in which the adjustments may be recognized. For the same reasons, the Company is unable to address the probable significant of the unavailable information, which could be material to future results. Adjusted Gross Profit and Adjusted Gross Profit Margin We believe that the presentation of Adjusted Gross Profit and Adjusted Gross Profit Margin is appropriate to provide additional information to investors about our gross profit adjusted for certain non-cash items. Further, we believe Adjusted Gross Profit provides a meaningful measure of operating profitability because we use it for evaluating our business performance, making budgeting decisions, and comparing our performance against that of other peer companies using similar measures. We define Adjusted Gross Profit as gross profit adjusted for (i) share-based compensation expense and (ii) depreciation and amortization. We define Adjusted Gross Profit Margin as Adjusted Gross Profit divided by Revenue. There are material limitations to using Adjusted Gross Profit and Adjusted Gross Profit Margin. Adjusted Gross Profit does not take into account all items which directly affect our gross profit. These limitations are best addressed by considering the economic effects of the excluded items independently and by considering Adjusted Gross Profit in conjunction with gross profit as calculated in accordance with GAAP. The Adjusted Gross Profit discussion above is also applicable to Adjusted Gross Profit Margin. Adjusted EBITDA and Adjusted EBITDA Margin We believe that the presentation of Adjusted EBITDA and Adjusted EBITDA Margin is appropriate to provide additional information to investors about our operating profitability adjusted for certain non-cash items, non-routine items that we do not expect to continue at the same level in the future, as well as other items that are not core to our operations. Further, we believe Adjusted EBITDA and Adjusted EBITDA Margin provide a meaningful measure of operating profitability because we use them for evaluating our business performance, making budgeting decisions, and comparing our performance against that of other peer companies using similar measures. We define Adjusted EBITDA as net income or loss adjusted for (i) interest, (ii) taxes, (iii) depreciation and amortization, (iv) share-based compensation expense, and (v) other non-recurring and/or non-cash items. We define Adjusted EBITDA Margin as Adjusted EBITDA divided by Revenue. There are material limitations to using Adjusted EBITDA and Adjusted EBITDA Margin. Adjusted EBITDA does not take into account certain significant items, including depreciation and amortization, interest, taxes, and other adjustments which directly affect our net income or loss. These limitations are best addressed by considering the economic effects of the excluded items independently and by considering Adjusted EBITDA in conjunction with net income or loss as calculated in accordance with GAAP. The Adjusted EBITDA discussion above is also applicable to Adjusted EBITDA Margin. Adjusted Free Cash Flow We believe that the presentation of Adjusted Free Cash Flow is appropriate to provide additional information to investors about our ability to service and repay debt and other payment obligations, make other investments, and pay dividends. We define Adjusted Free Cash Flow as cash flows from operating activities less cash outlays related to capital expenditures (which primarily relate to purchases of property, plant and equipment) adjusted for other payments or receipts that may mask our operating results or business trends. As a result, subject to the limitations described below, Adjusted Free Cash Flow is a useful measure of our cash flow attributable to our normal business activities, as well as our ability to service and repay debt and other payment obligations, make other investments, and pay dividends. Adjusted Free Cash Flow adjusts for cash items that are ultimately within management’s discretion to direct, and therefore, may imply that there is less or more cash that is available than the most comparable GAAP measure. Adjusted Free Cash Flow is not intended to represent residual cash flow for discretionary expenditures since debt repayment and other payment obligation requirements and other non-discretionary expenditures are not deducted. These limitations are best addressed by using Adjusted Free Cash Flow in combination with the GAAP cash flow numbers. Unlevered Adjusted Free Cash Flow We define Unlevered Adjusted Free Cash Flow as Adjusted Free Cash Flow adjusted for cash interest paid. As a result, subject to the limitations described below, Unlevered Adjusted Free Cash Flow is a useful measure of our cash available to service and repay debt and other payment obligations, make other investments, and pay dividends. Unlevered Adjusted Free Cash Flow adjusts for contractual interest and other obligation payments as well as cash items that are ultimately within management's discretion to direct, and therefore, may imply that there is less or more cash that is available than the most comparable GAAP measure. Unlevered Adjusted Free Cash Flow is not intended to represent residual cash flow for discretionary expenditures since debt repayment and other payment obligation requirements and other non-discretionary expenditures are not deducted. These limitations are best addressed by using Unlevered Adjusted Free Cash Flow in combination with the GAAP cash flow numbers. Source: Company management. |

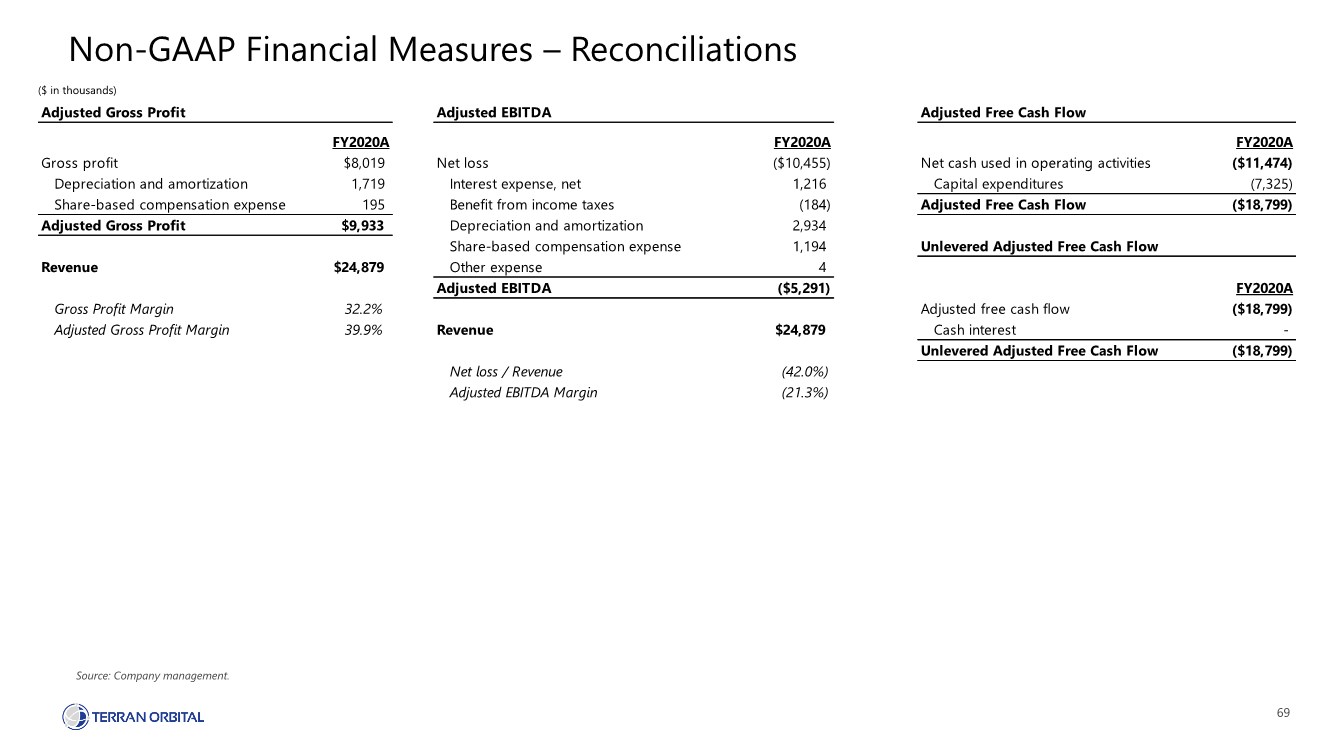

| 69 Non-GAAP Financial Measures – Reconciliations Source: Company management. ($ in thousands) Adjusted Gross Profit Adjusted EBITDA Adjusted Free Cash Flow FY2020A FY2020A FY2020A Gross profit $8,019 Net loss ($10,455) Net cash used in operating activities ($11,474) Depreciation and amortization 1,719 Interest expense, net 1,216 Capital expenditures (7,325) Share-based compensation expense 195 Benefit from income taxes (184) Adjusted Free Cash Flow ($18,799) Adjusted Gross Profit $9,933 Depreciation and amortization 2,934 Share-based compensation expense 1,194 Unlevered Adjusted Free Cash Flow Revenue $24,879 Other expense 4 Adjusted EBITDA ($5,291) FY2020A Gross Profit Margin 32.2% Adjusted free cash flow ($18,799) Adjusted Gross Profit Margin 39.9% Revenue $24,879 Cash interest - Unlevered Adjusted Free Cash Flow ($18,799) Net loss / Revenue (42.0%) Adjusted EBITDA Margin (21.3%) |